Thinking of launching a crowdfunding platform in the UAE? The Dubai International Financial Centre (DIFC) offers a regulated framework for investment, loan, and property-based crowdfunding. Here's what you need to know:

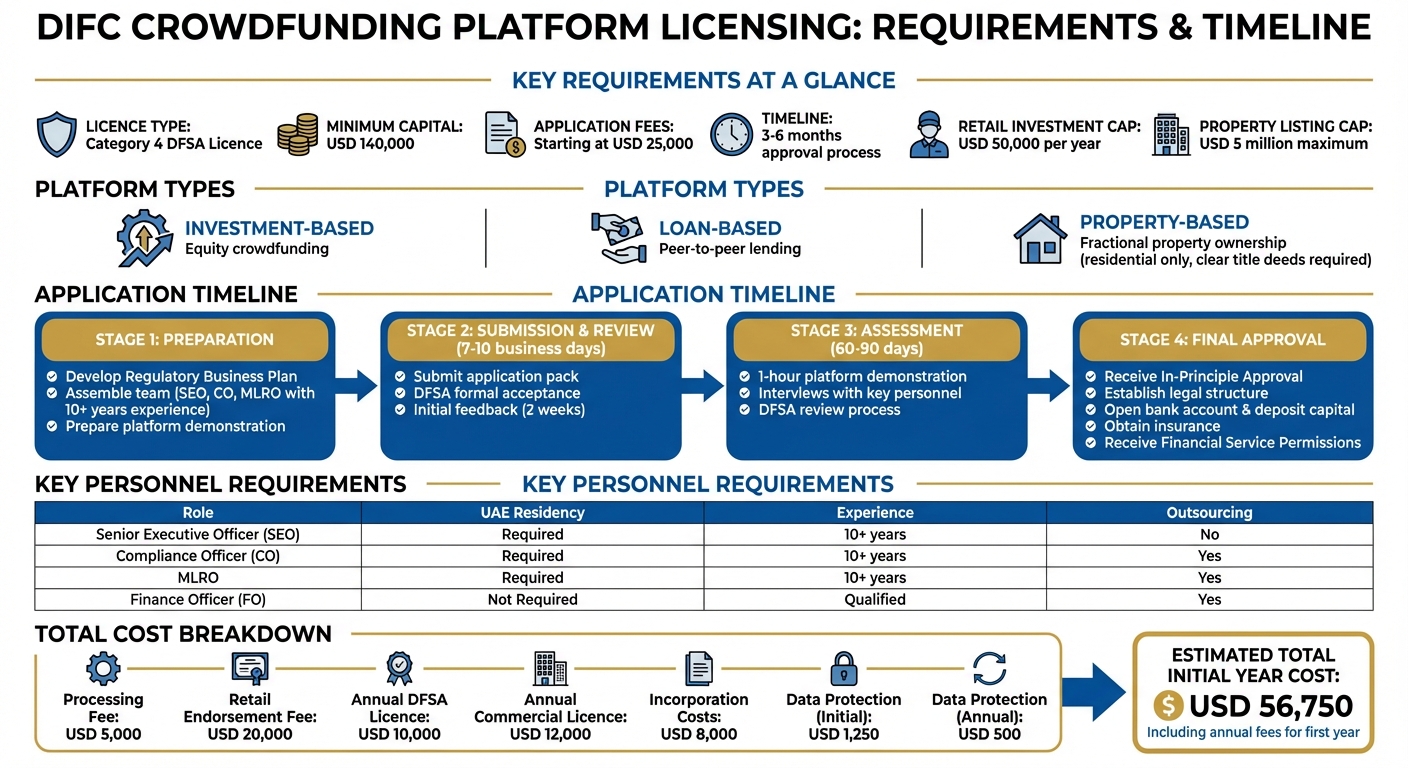

Timeline: The approval process takes 3–6 months, including a detailed application review, platform demonstration, and regulatory interviews.

Setting up a DIFC-compliant crowdfunding platform requires preparation, compliance, and a strong team. Staying updated on the latest UAE startup news can help founders navigate these regulatory shifts. While the process is detailed, it ensures trust and transparency for operators and investors alike.

DIFC Crowdfunding Platform Licensing Process Timeline and Requirements

Getting a DFSA licence involves more than just registering your business - it’s a detailed approval process. The DFSA classifies crowdfunding businesses as Category 4 entities, with their main activity defined as "Operating a Crowdfunding Platform" [1][2]. The review process usually takes between 60 and 120 days after the formal application is submitted [1][2]. Here's what you need to know to prepare effectively.

The DFSA recognises three main types of crowdfunding platforms: investment-based (equity crowdfunding), loan-based (peer-to-peer lending), and property-based (fractional property ownership) [1][2]. If you're considering a property-focused platform, note that only residential properties with clear title deeds are allowed - commercial properties and off-plan developments are excluded [2]. Additionally, property listings are capped at a maximum value of US$ 5 million [2].

Your Regulatory Business Plan (RBP) is a critical document. It must outline your business model, market strategy, and detailed financial projections, which help determine your capital requirements. The plan should also include your organisational structure, such as the Board of Directors and key operational roles [1][4].

You’ll need to document operational policies, risk management procedures, and compliance measures, with a particular focus on KYC (Know Your Customer) and AML (Anti-Money Laundering) protocols [6][3].

Key personnel are essential:

Additionally, the RBP must include four risk disclosure statements on your platform’s website, warning investors about potential capital loss and the high failure rate of startups [3].

One unique requirement is the live platform demonstration. As part of the review, you’ll need to provide a one-hour technical walkthrough of your platform to the DFSA, showcasing its functionality and compliance with their standards [1][2]. Once your RBP is complete, you can focus on meeting capital and fee requirements.

The base capital requirement is US$ 140,000, but the final amount depends on the highest of three calculations: base capital, risk-based capital, or expense-based capital [1][2]. For platforms handling client funds, expense-based capital is calculated as 18/52 of projected annual expenses [1][2]. Your financial projections in the RBP will help determine which amount applies.

Fees include:

After the DFSA reviews your application, interviews with your SEO, FO, and CO/MLRO will follow. A successful review results in In-Principle Approval (IPA) [1]. At this stage, you’ll need to finalise your legal structure, open a UAE bank account, deposit the required share capital, and secure professional indemnity insurance before receiving your final Financial Services Permission [1].

After securing In-Principle Approval, the next step is to focus on implementing measures that ensure investor protection. The DFSA places a high priority on safeguarding investors, so your procedures need to meet stringent standards right from the start. This includes adhering to mandatory KYC, AML, and risk disclosure protocols.

As outlined in your Regulatory Business Plan, it's essential to establish strong Customer Due Diligence (CDD) processes to verify the identities and legal credentials of both borrowers and issuers [3].

Identifying the Ultimate Beneficial Owner (UBO) is a critical requirement. This involves verifying any individual who owns or controls at least 25% of an entity [7]. Additionally, Source of Funds (SoF) verification is crucial. According to the DIFC Authority:

"Source / origin of funds or income refers to the origin of the particular funds or assets which are the subject of the business relationship... The information obtained should be substantive, relevant and able to establish the fund's origin." [7]

This means conducting thorough checks to confirm the legitimacy of the funds' origin [7]. You are also required to screen for Politically Exposed Persons (PEPs), including their family members and close associates, due to their heightened risk of involvement in money laundering or corruption [7]. Risk assessments should take into account factors such as the source of funds, business location, and activities [7]. Automated tools that reference indices like the Basel AML Index and the Transparency International Corruption Index can help identify country-specific risks [7].

The DFSA mandates that your platform display four explicit risk warnings to investors, highlighting potential capital loss, high startup failure rates, illiquidity, and platform closure risks [3]. Additionally, you must disclose historical data on loan default rates and issuer failure rates [3].

Once your compliance measures are in place, the next step is to classify investors as either Retail or Professional under DFSA regulations [6]. Retail clients must have a US$ 20,000 endorsement; without this, only professional investors can participate [1][2].

Retail investors are subject to stricter limits, particularly in property crowdfunding, where the maximum investment is capped at US$ 50,000 per calendar year [1][2]. Professional investors, on the other hand, typically have fewer restrictions [6].

| Feature | Retail Investors | Professional Investors |

|---|---|---|

| Investment Limit | US$ 50,000 per calendar year [1][2] | Generally higher/unrestricted access [6] |

| Platform Requirement | Requires "Retail Endorsement" [1] | Standard licensing applies [6] |

| Disclosure Focus | High; requires clear understanding of risks [8] | Standard professional disclosures |

| Property Cap | US$ 5 million max listing value [2] | N/A |

The DFSA's Conduct of Business (COB) rules are designed to ensure transparency and fairness in platform operations. Your client agreements must be clear and standardised. A 2024 DFSA review highlighted common compliance gaps, such as incomplete information in client agreements and weak controls for reviewing disclosures [8]. It is important not to disclaim liability for platform-disclosed information [8].

Your platform's operating model must be fully transparent. This includes explaining how the platform functions, how fees and charges are structured, and the eligibility criteria for borrowers and lenders [3]. For each listing, provide detailed due diligence results, including the borrower's financial health, credit history, and a comprehensive description of the funding proposal. This should also cover how funds will be used and plans for handling over-funding or under-funding scenarios [3].

For property crowdfunding, only residential properties with clear title deeds are allowed, and off-plan properties are strictly prohibited [2]. Property listings must not exceed US$ 5 million [2]. If there are significant changes in a borrower's circumstances, such as a management overhaul or asset restructuring, you are required to notify investors immediately and seek their reconfirmation [3]. Additionally, your client agreements should include clear mechanisms for dispute resolution and grievance handling to comply with DFSA rules [4][6].

Once you've met the licensing and compliance requirements, the next step is to align your operational and governance standards with the expectations of the DFSA. This involves setting up strong operational procedures, implementing thorough risk management systems, and ensuring accountability at every organisational level.

Your crowdfunding platform must rely on digital channels for key functions like client onboarding and transaction processing. However, all client-facing activities and core operations need to be conducted from your firm's premises in the DIFC to meet local licensing rules.

Key personnel appointments are crucial. The Senior Executive Officer (SEO) must reside in the UAE, have at least 10 years of experience, and cannot be outsourced. Similarly, the Compliance Officer (CO) and Money Laundering Reporting Officer (MLRO) must each have over 10 years of experience. These roles can be combined and outsourced if necessary. A Finance Officer (FO) is also required, but this individual does not need to be UAE-based if your firm is part of a larger group. The DFSA allows outsourcing for the CO, MLRO, and FO roles when appropriate.

To address operational risks, you’ll need systems that can identify and mitigate them effectively. While a dedicated Risk Officer is not mandatory, this function is often outsourced for independent oversight. Importantly, staff members are prohibited from participating on the platform as lenders, investors, borrowers, or issuers to maintain fairness and transparency [3]. With these measures in place, you can ensure operational risks are well-managed and regulatory compliance is upheld.

The DFSA requires a well-structured Board with clear governance policies. The Board’s Chair must be a Non-Executive Director (NED) to ensure impartial oversight. Additionally, you will need both internal and external auditors. While the internal auditor role is typically outsourced, the external auditor must be selected from the DFSA’s approved list of firms. Confirm your chosen auditor’s status on this list to avoid compliance delays.

| Role | Residency Requirement | Experience Requirement | Outsourcing Permitted |

|---|---|---|---|

| Senior Executive Officer (SEO) | UAE Resident | 10+ Years | No |

| Compliance Officer (CO) | UAE Resident | 10+ Years | Yes |

| MLRO | UAE Resident | 10+ Years | Yes |

| Finance Officer (FO) | Not Required | Suitably Qualified | Yes |

| Risk Officer | Not Required | Suitably Qualified | Yes (Usually Outsourced) |

| Internal Auditor | Not Required | Suitably Qualified | Yes (Usually Outsourced) |

You are required to submit auditor reports to the DFSA within four months of your financial year-end, as specified under Rule GEN 8.6.2 [5]. For example, in July 2020, the DFSA extended this deadline to eight months for FundedByMe MENA Limited due to unique circumstances related to the financial year ending between 31 December 2019 and 31 March 2020 [5]. While such extensions may be granted in exceptional cases, it’s best not to depend on this flexibility. Beyond internal oversight, your external communications and client service protocols should also demonstrate a strong commitment to transparency.

The DFSA enforces strict marketing rules. You are prohibited from advertising specific lending or investment opportunities to non-clients, as this could be considered an "offer of securities to the public", which would require a prospectus [3]. Instead, your marketing efforts should focus on promoting your platform as a whole rather than individual listings.

Transparency is key in your operating model. You must clearly outline how your platform earns revenue, the eligibility criteria for users, and any limits on loans or investments [3]. Additionally, you are required to publicly disclose default rates for loans and failure rates for issuers, giving potential investors a clear view of historical performance.

Before scheduling your one-hour DFSA demonstration, ensure your platform is fully operational and compliant with all these requirements.

The licensing process typically takes 3–6 months from the initial submission to final approval. However, the duration may vary depending on how detailed and complete your application is. This timeline assumes that all capital, compliance, and governance requirements have been addressed, as outlined earlier. Below is a breakdown of the key stages involved, from submission to receiving final approval.

The process begins with formal introductions to the DIFC and DFSA. Following this, you'll need to prepare your Regulatory Business Plan (RBP) and financial projections. Once your application pack is ready - including the RBP, policies, processes, and KYC forms for key personnel - it is submitted to the DFSA. The regulator reviews the submission within 7–10 business days before formally accepting it [1]. Regular communication with the DFSA is maintained throughout, and initial feedback is typically provided about two weeks into the review [1].

The assessment phase follows, lasting between 60 and 90 days [1]. During this time, you’ll be required to conduct a one-hour platform demonstration and attend interviews with key personnel, such as your Senior Executive Officer, Finance Officer, and Compliance/Money Laundering Reporting Officer [1]. It’s crucial that your team is well-prepared and available for these steps.

If successful, you’ll receive in-principle approval. From there, you must meet specific conditions, including establishing your legal structure with the DIFC Registrar of Companies, opening a corporate bank account, depositing the required share capital (a minimum of US$ 140,000 for Category 4 licences), finalising agreements with auditors, and obtaining Professional Indemnity Insurance [1][2]. Once these steps are completed, you can finalise your submission to secure Financial Service Permissions.

Setting up a crowdfunding platform in DIFC comes with a structured regulatory framework designed to safeguard both operators and investors. To start, you’ll need to secure a Category 4 licence, which requires a minimum capital of US$ 140,000. Additionally, you must appoint UAE-based SEO and compliance officers with over 10 years of experience, establish strong KYC/AML protocols, and pass a one-hour live demonstration with the DFSA. Be prepared to budget around US$ 25,000 for application fees as part of the process. These steps are critical for navigating the extensive DFSA review.

Planning ahead is key. The DFSA review process can take anywhere from 60 to 120 days, so it’s important to have your capital and team in place early. Keep in mind that there are specific restrictions, such as retail investments being capped at US$ 50,000 per year and property listings limited to US$ 5 million. These limits will play a crucial role in shaping your market strategy and revenue forecasts from the outset.

Beyond regulatory compliance, leveraging community networks can give you a competitive edge. UAE fintech startups can tap into resources like Founder Connects, which provides virtual masterminds, networking opportunities, and curated access to investors. This can be particularly helpful when recruiting qualified individuals for mandatory roles or gaining insights into the DFSA application process.

While the regulatory requirements may seem daunting, they offer a significant advantage: credibility with investors. As one fintech founder highlighted, demonstrating strong regulatory compliance can fast-track funding opportunities. For UAE tech and fintech startups, this credibility often outweighs the initial compliance costs, paving the way for sustainable growth within the dynamic UAE startup ecosystem.

To obtain a DFSA licence for your crowdfunding platform in DIFC, here’s what you need to do:

Once your application is approved, you’ll be officially authorised to run your crowdfunding platform in DIFC, playing a vital role in the UAE’s thriving startup ecosystem.

The DIFC regulations, under the watchful eye of the DFSA, are designed to protect investors by ensuring crowdfunding platforms meet licensing requirements and follow a clear regulatory framework. These rules mandate the disclosure of critical information, the segregation of investor funds, and rigorous anti-money laundering (AML) checks.

On top of this, the DFSA maintains ongoing oversight to ensure these platforms remain transparent and operate with integrity. This approach not only safeguards investors but also strengthens confidence in the UAE's startup ecosystem.

The DFSA mandates applicants for a DIFC crowdfunding platform licence to provide comprehensive details about their governance structure and senior management team. However, the summaries of the DFSA rulebook do not specify exact qualifications, years of experience, or professional backgrounds required for key roles such as CEO, compliance officer, or risk-management officer.

To stay on the safe side and meet all requirements, it’s advisable to carefully review the full DFSA COB-11 Crowdfunding rulebook. Alternatively, seeking guidance from a regulatory expert can provide clarity and help ensure the licensing process proceeds without complications.