Network International Payment Solutions: A Founder's Guide

That first international order feels like validation. It also creates immediate operational pressure. You need to accept payment cleanly, settle funds reliably, reconcile them in your books, and make sure the next ten orders don't break because your gateway setup was rushed.

For founders in the UAE and wider MENA region, that decision gets complicated fast. Local banks, cross-border card flows, fraud controls, VAT workflows, settlement timing, and accounting integrations all show up earlier than expected. Network International payment solutions come up quickly in that conversation for a reason. Network International was founded in 1994 and is the largest acquirer in the UAE, processing over $59 billion in payment volumes in 2023 for more than 130,000 merchants across MEA, according to Network International's company overview.

The scale is reassuring. Scale alone doesn't solve founder problems.

What matters is whether the product fits your business model, your technical resources, your fraud profile, and your finance team's reality. This guide looks at Network International the way a founder should. Not as a logo on a pitch deck, but as an operating decision with trade-offs.

Your First International Sale Is In Now What

The first problem isn't getting paid once. It's building a payment setup that still works when orders start coming from different countries, cards fail for inconsistent reasons, and your accountant asks why settled amounts don't match checkout totals.

A lot of founders treat gateway selection like a website plugin choice. That's too shallow. Payment infrastructure affects cash flow, conversion, fraud exposure, support workload, and investor confidence. If customers can't pay, growth stalls. If settlements are messy, finance loses time every week. If fraud controls are blunt, good customers get blocked.

Network International deserves attention because it isn't a niche processor. It's a regional heavyweight with deep market presence in the UAE and across MEA. That matters when you're selling into markets where local relationships, acquiring strength, and operational support can matter as much as the API itself.

What makes this decision strategic

At the start, most founders only ask three questions:

- Can I accept cards

- How much are the fees

- How long will integration take

Those questions matter, but they aren't enough. You also need to know:

- Where you'll sell next: GCC only, broader MENA, Europe, or beyond.

- How customers will pay: one-off card payments, subscriptions, invoices, POS, or some mix.

- Who owns the edge cases: failed payments, disputes, refunds, reconciliation, fraud reviews.

- What breaks under growth: checkout reliability, reporting, team workflows, or ERP sync.

Practical rule: Choose for the next stage of your company, not just the next transaction.

If you're still sorting out your banking structure, it's worth reading this UAE banking guide for pre-seed startups before you commit to any payment stack. Banking setup and gateway setup usually collide.

A useful founder mindset

Don't ask, "Is Network International good?"

Ask, "Is it good for my payment model, team size, and target markets?"

That shift changes the whole evaluation. A B2C ecommerce brand has different needs from a SaaS company billing subscriptions in multiple currencies. A marketplace has different risk and reconciliation complexity from a consulting firm sending payment links.

If part of your customer base includes UK buyers or entities, this practical breakdown on handling international transactions for UK companies is worth reviewing alongside your local setup. It helps frame where card gateways fit versus broader international payment rails.

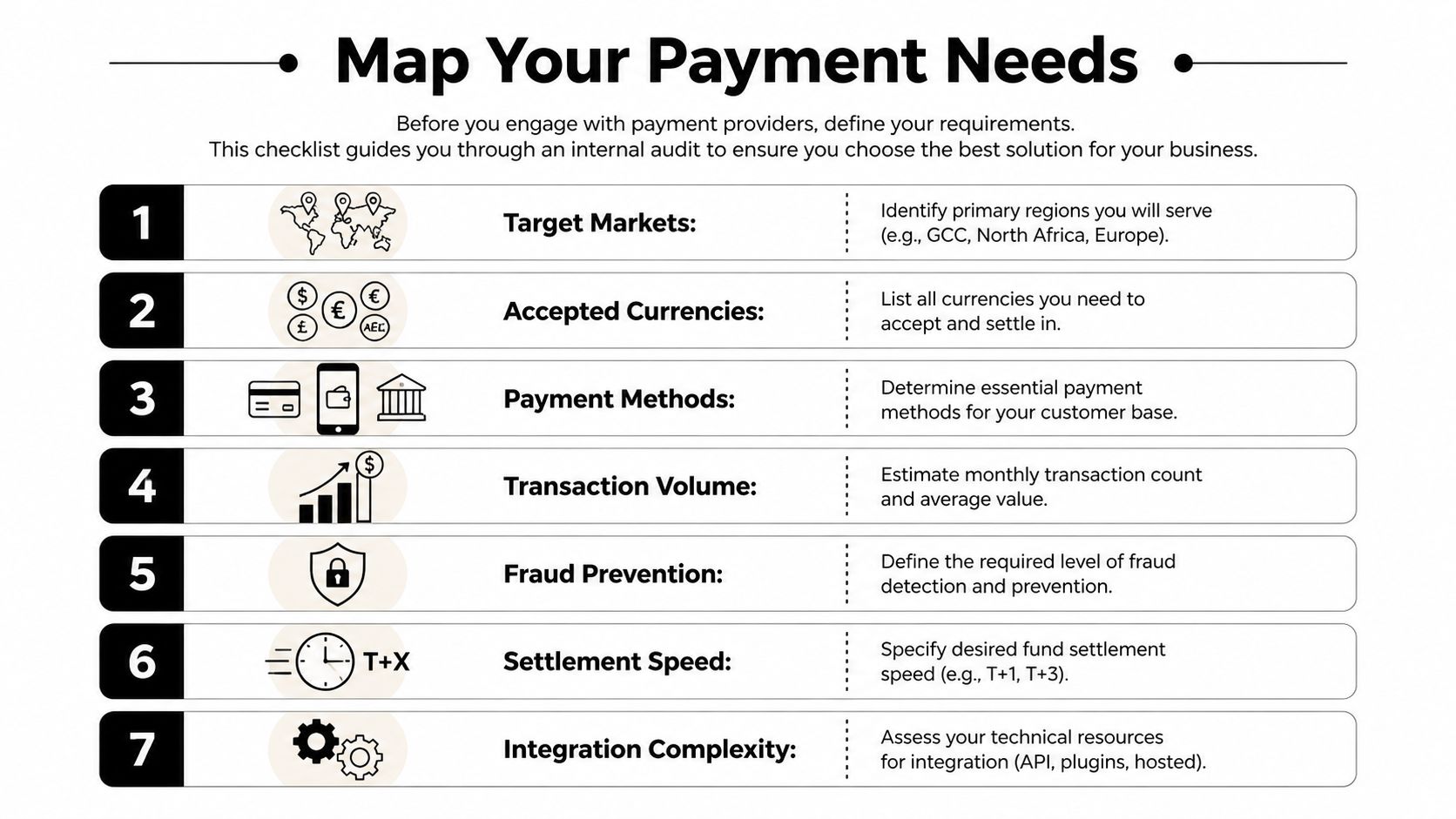

Map Your Payment Needs Before Talking to Sales

Most sales calls go wrong before they start. The founder shows up with vague needs, the provider shows a broad product deck, and everyone leaves feeling progress was made. Then integration begins and the mismatches appear.

Start internally. Write a one-page payment requirements document before you book any demo.

The internal audit that saves time later

Network International isn't just a gateway. In the Middle East, 51% of its business comes from Outsourced Payment Services, and its network services over 200 banks and 70,000+ merchants, according to this company profile. That scale can be useful if you're building for regional reach, but only if your requirements are clear enough to evaluate the right parts of the stack.

Get your founder, finance lead, and whoever owns product or engineering into one discussion. Work through these questions.

Commercial questions

- Where are customers today: UAE only, GCC, wider MENA, or mixed international.

- What are you selling: physical goods, software subscriptions, services, travel, events, or invoices.

- How do people pay: checkout page, payment link, recurring billing, POS terminal, or account-to-account flows.

- What settlement pattern do you need: fast operating cash for payroll and ads, or can finance tolerate slower cycles.

Operational questions

- Who handles refunds: operations, support, or finance.

- How are disputes tracked: inside the gateway dashboard, in CRM notes, or manually in spreadsheets.

- Which tools must connect: ERP, accounting software, CRM, subscription platform, or custom backend.

- What reporting granularity matters: daily settlements, transaction-level exports, VAT handling, or payout reconciliation.

If your team can't explain your payment flow on one page, you're not ready for a sales demo.

Turn your needs into must-haves and nice-to-haves

Use a simple split:

| Category | Must-have | Nice-to-have |

|---|---|---|

| Markets | Current sales geographies supported | Future expansion corridors |

| Payment flow | Core checkout or invoicing model | Edge channels you may test later |

| Integration | Works with your existing finance stack | Deeper automation later |

| Risk | Fraud tools matched to your category | Advanced tuning once scale justifies it |

This sounds basic, but it prevents a common founder mistake. Teams buy based on feature breadth, then realise the day-to-day experience isn't built around their actual operations.

A finance-led framework also helps. If you want a sharper lens for cost control, ownership, and internal approval, this CFO's guide to payment gateways is useful reading before you compare providers.

For regional context, it also helps to understand how payment providers fit into the wider ecosystem of banks, fintechs, and partners. This overview of UAE fintech collaborations and key players gives that broader picture.

Uncover the Real Costs Beyond Transaction Fees

Transaction fees are the most advertised part of any gateway deal. They are rarely the most expensive part of the decision.

The hidden cost problem is especially real for founders integrating payment solutions into messy operational stacks. You may save on headline pricing and then lose that saving through consultant fees, delayed launch, manual reconciliation, and finance team workarounds.

A useful reality check comes from the business payments angle. A 2024 UAE Central Bank report noted that 42% of SMEs face integration delays exceeding three months because of API mismatches, and a 2025 DIFC fintech survey found integration consultants cost an average of AED 15,000 per setup, as referenced in the discussion around Network International Business Payment Solutions. That's the part many founder budgets miss.

What founders often forget to price in

The main fee is only one line item. Ask about these before you sign:

- Setup work: internal engineering time, implementation support, plugin limitations, and testing cycles.

- Finance overhead: who reconciles settlements, fees, refunds, and chargebacks each week.

- Accounting integration: whether your existing ERP or accounting workflow needs custom mapping.

- Support costs: how payment failures land on your support team.

- Contract friction: minimum commitments, lock-in periods, and escalation terms.

Hidden costs show up in operations first

A founder usually sees the issue in one of three places.

First, your engineer says the API is workable, but finance still can't reconcile settlements cleanly.

Second, your accountant starts exporting CSV files and patching gaps manually.

Third, you discover that "integration support" means hiring an outside specialist because your stack doesn't fit the standard path.

Cheap processing becomes expensive when your team has to babysit the system.

This is also where FX deserves more attention than it gets. Even if a provider markets cross-border capability well, founders should understand where conversion costs can sit inside the payment flow. This explainer on FX trading spread is helpful if you want a cleaner view of how spreads subtly influence unit economics.

Questions to ask Network International before signing

Don't ask for a generic pricing sheet and stop there. Ask these directly.

- Integration scope: What does the standard integration include, and what usually falls outside it?

- Accounting fit: Which ERP and accounting workflows are straightforward, and which tend to need custom work?

- Settlement reporting: How will finance match orders, settlements, refunds, and fees without manual intervention?

- Support model: Who handles urgent payment issues after go-live, and how are escalations routed?

- Contract terms: Are there minimums, implementation charges, or dependencies that change the commercial model later?

This short explainer is worth watching before you negotiate. It helps frame how gateway pricing and payment operations often diverge in practice.

A simple decision test

If you're comparing providers, build a sheet with three columns:

| Cost area | Visible in proposal | Usually discovered later |

|---|---|---|

| Processing fees | Yes | Sometimes |

| Integration work | Sometimes | Often |

| Reconciliation effort | Rarely | Often |

| Consultant support | Rarely | Often |

| Team time during launch | No | Yes |

That exercise changes the conversation. You're no longer buying a rate. You're buying an operating model.

Your Technical Integration and Testing Checklist

Good gateway decisions can still go sideways. The commercial team signs. Engineering gets API docs. Everyone assumes launch is a matter of wiring up checkout and switching to production.

It isn't.

Improper retry logic and integration errors can cause 15-25% of payments to fail artificially, and businesses that segment failure codes and use intelligent retries such as 1, 5, and 15-minute intervals for network errors have seen success rates improve by 12-18%, according to this breakdown of payment success rate optimisation.

The checklist founders should manage personally

You don't need to write the code. You do need to own the checklist.

Sandbox first, production later

Make sure your team has a complete test environment before touching live traffic. That includes:

- API access: sandbox keys, role permissions, and clear ownership.

- Test cases: approvals, declines, refunds, duplicate attempts, and timeout scenarios.

- Webhook handling: every payment event should be captured, logged, and visible somewhere your team can review.

Failure codes matter more than founders expect

Not all failed payments mean the same thing.

A soft decline might be a timeout or temporary network issue. A hard decline might indicate a non-retriable failure. If your system treats both the same, you lose recoverable revenue and frustrate customers.

Use a simple internal rule set:

- Retry technical failures: timeouts and transient network issues.

- Don't retry everything: insufficient funds or clearly terminal failures need a different customer prompt.

- Log the reason cleanly: support and product teams need visibility.

The dashboard number that matters isn't just "payments failed". It's "which failures were actually recoverable".

How to measure the true success rate

Many teams inflate performance without meaning to. They count successes against a partial set of attempts, or they ignore retries when they present metrics internally.

A better founder view includes:

- All attempts counted: first try plus any retry attempts.

- Matched time periods: don't compare one day's successes against a different attempt window.

- Failure segmentation: technical, customer-driven, fraud-related, and unknown.

That lets you answer the only question that matters after launch. Did customers who intended to pay get through?

Test the edge cases before launch

Run live-like tests across actual payment paths you plan to support.

| Test area | What to confirm |

|---|---|

| Checkout flow | Customer can complete payment without confusion |

| Retry handling | Temporary failures recover correctly |

| Refund flow | Finance and support can process and track it |

| Notifications | Customer and internal teams get the right updates |

| Reporting | Transactions appear correctly in the dashboard and exports |

Don't let engineering sign off alone. Ask finance to review reports and ask support to walk through a failed payment scenario. That catches the practical problems that code review won't.

Mitigating Fraud and Regulatory Risks in MENA

A gateway can process payments well and still leave you exposed. That usually happens when founders treat fraud and compliance as add-ons instead of operating requirements.

In MENA, you need a setup that recognises local transaction patterns, not just generic global fraud templates. Network International's implementation of FICO Falcon Fraud Manager is a strong example of that approach. According to FICO's announcement on the deployment, the system achieved a fraud detection rate exceeding 90% across payment channels using machine learning models trained on MEA-specific transaction patterns.

Why regional context matters in fraud controls

Founders often underestimate how quickly fraud tooling becomes a growth issue. If controls are too loose, bad actors get through. If controls are too aggressive, legitimate customers are blocked and support queues fill up.

The practical value in a system like Falcon isn't just the headline detection rate. It's the operating model behind it:

- Real-time scoring: decisions happen during authorisation, not after the loss.

- API-based integration: payment events can be assessed without bolting on a separate manual layer.

- Local pattern recognition: the model is trained around regional transaction behaviour rather than relying only on generic assumptions.

That last point matters. Cross-border B2B payments, changing device behaviour, and uneven customer histories across markets can make blunt global rules perform badly in this region.

What a founder should ask for

When evaluating fraud controls inside network international payment solutions, ask specific operational questions.

- How are transactions scored in real time

- What fields or behaviours drive manual review

- How can we tune rules by market or product line

- What is the process for reducing false positives after launch

- Who owns the fraud review queue internally

If the answer is just "we have advanced fraud protection", keep digging.

A good fraud stack blocks bad payments. A better one also preserves good revenue.

Compliance is part of the same conversation

Fraud and compliance usually break in the same week. Once you start taking money across borders, customer verification, record-keeping, internal controls, and escalation processes become more important. Founders building products with embedded finance, stored value, remittance elements, or regulated payment flows need to take that even more seriously.

This practical guide to building regulated financial products in the UAE is worth reviewing if your model sits anywhere near regulated activity.

A few working rules help:

- Document who reviews exceptions: don't leave suspicious activity decisions floating between ops and finance.

- Separate growth from risk ownership: the team pushing conversion shouldn't be the only team deciding fraud tolerances.

- Keep an audit trail: approvals, reversals, and manual reviews should be visible later.

What works in practice

The strongest setups usually share the same traits:

| Area | What works | What fails |

|---|---|---|

| Fraud monitoring | Real-time scoring with local tuning | Static rules left untouched |

| Escalation | Clear owner and response path | Shared inbox chaos |

| Customer review | Structured manual checks | Ad hoc judgement |

| Compliance records | Searchable logs and policy discipline | Scattered screenshots and email trails |

For an early-stage founder, the key is simple. Don't wait for your first fraud incident or bank query to define your process for you.

The Founder's Go-Live and Launch Day Checklist

Launch day problems are rarely dramatic at first. They show up as small failures. A customer says their card didn't go through. A payout report doesn't match orders. Support asks who owns refunds. Finance sees a discrepancy and engineering says the logs look fine.

That's why a go-live checklist matters. It reduces preventable confusion.

Final checks before you switch to production

Run through these as a team, not in separate silos.

- Production credentials confirmed: make sure live API keys, webhooks, and permissions are in the correct environment.

- A real payment tested: put one controlled live transaction through the full journey from checkout to settlement visibility.

- Refund path verified: confirm both the technical flow and the internal approval process.

- Customer communication ready: receipts, failure messages, and support replies should be clear and accurate.

- Dashboard access assigned: finance, ops, support, and engineering should each have the access they need.

Support readiness matters

A good launch isn't just a technical milestone. Your customer-facing team needs scripts for common cases:

- Payment pending

- Card charged but order not confirmed

- Refund requested

- Repeated failed attempts

- Suspected fraud or blocked transaction

Write the responses before launch. Keep them short. Include the internal escalation owner beside each one.

Launch day gets easier when every payment problem already has an owner.

What to watch in the first days

You don't need a huge war room. You do need rhythm.

Use a simple monitoring cadence for the first stretch after launch:

| Time window | What to review |

|---|---|

| First few hours | Successful payments, obvious failures, webhook events |

| End of day | Refund flow, reporting quality, support tickets |

| Following days | Recurring failure patterns, dispute signals, finance reconciliation |

Look for patterns, not isolated noise. One failed card doesn't mean much. Repeated failures on a specific flow, market, or device type usually mean something is off.

A founder's short punch list

Print this and keep it visible.

- Confirm live environment settings

- Run one real end-to-end payment

- Check settlement visibility

- Verify refund and cancellation handling

- Review customer emails and on-site error messages

- Make sure support knows escalation routes

- Have finance review the first reporting export

- Schedule daily launch check-ins until the flow is stable

The founders who avoid messy payment launches don't have magic providers. They force clarity before traffic arrives.

If you're implementing network international payment solutions, that discipline matters even more because the product can be powerful, but only if your commercial setup, technical integration, finance workflow, and risk controls all line up. That's the key decision. Not whether the provider is credible. Whether your team is ready to use it well.

If you want founder-level help pressure-testing decisions like payment providers, banking setup, fintech tooling, or launch readiness, Founder Connects is built for exactly that. It's a UAE-rooted founder community where operators compare notes openly, make warm introductions, and help each other avoid expensive mistakes before they happen.

Popular posts

The premier community for tech founders, investors, and builders. Connect, collaborate, and grow together.