Business Brokers in Dubai: Your Guide to Selling a Business

Building in MENA? You don't have to do it alone.

Join 300+ founders in the Founder Connects Residency. Monthly squad calls, warm intros, $3M+ in perks, and much more. All for less than your monthly coffee budget.

You've built something that works. Revenue is coming in. The team knows how to deliver. Then the question lands. Should you sell now, test the market, or wait?

In Dubai, that decision gets complicated fast. A business sale here isn't just about finding someone who likes your company. It's about licences, approvals, buyer credibility, payment structure, handover risk, and whether the intermediary sitting between you and the buyer can close a deal.

That's where many founders lose time. They assume a broker's job is to “market the business”. In practice, their primary role is managing a fragile process without leaking confidential information, attracting the wrong buyers, or agreeing terms that collapse later.

A lot of generic advice online misses the UAE reality. Dubai is a strong commercial hub, but it's not a copy of London, Singapore, or New York. The mechanics are different. Financing is different. Administrative dependencies are different. The broker you choose can either reduce those risks or amplify them.

Why You Need a Playbook for Selling Your Business in Dubai

Most founders only sell a business once, maybe twice. That makes it easy to underestimate how exposed you are when you enter the market unprepared.

The first risk is confidentiality. If staff, suppliers, landlords, or competitors hear about a sale too early, you can create operational noise before you've even found a serious buyer. The second risk is process drift. Without a clear sequence, valuation discussions turn vague, buyers ask for everything at once, and momentum disappears. The third risk is local execution. In Dubai, closing often depends on more than a signed SPA.

What founders usually get wrong

Founders often start with the wrong question. They ask, “Who is the biggest broker?” The better question is, “Who can take my specific company through a clean process in my specific jurisdiction?”

A sale of a mainland operating company isn't handled the same way as a free zone entity with approvals, visas, banking arrangements, and operational dependencies tied to the transfer. A buyer can be enthusiastic and still fail if nobody has mapped the practical steps properly.

Practical rule: Don't hire a broker because they promise buyers. Hire them because they can control the process from first conversation to transfer completion.

That's also why some founders bring in transaction support before they formally go to market. If you need help thinking through valuation positioning, buyer strategy, or deal readiness, it's worth reviewing Smart Classic Business Hub's services as one example of advisory support that sits closer to transaction execution than generic lead generation.

The playbook mindset

A useful playbook is simple:

- Get clear on your objective. Full exit, partial exit, strategic buyer, family office, operator-buyer, or quiet market test.

- Prepare buyer-ready information. Clean financials, licence details, ownership records, contract summaries, and a realistic explanation of growth and risk.

- Choose the intermediary based on execution fit. Sector fit matters. Jurisdiction fit matters more than most founders realise.

- Control disclosure. Information should move in stages, not all at once.

- Treat closing as a project. The deal isn't done when terms are agreed. It's done when ownership transfer, approvals, and handover are complete.

That discipline matters more in Dubai than polished sales talk.

What a Dubai Business Broker Really Does

A proper business broker is not a classifieds agent with a buyer list. The role is closer to a transaction manager who controls information, pressure-tests buyer quality, and keeps the deal moving when the easy part is over.

The difference matters because the wider brokerage industry is fragmented. Marketdata Enterprises says the business brokers market includes more than 1,500 brokerage firms and 8,000 brokers, and found that 30%–40% of brokers listed on BizBuySell are real estate agents rather than dedicated business brokers, according to Marketdata's industry analysis covered by WebWire. That's a useful warning for founders in Dubai. You need to verify whether the person pitching you specialises in business sales.

The real value sits in the middle of the process

Anyone can tell you your business is attractive. A good broker does harder work:

- Frames valuation properly so the price is defendable and not just aspirational.

- Prepares sale materials that answer serious buyer questions without exposing sensitive data too early.

- Runs confidential outreach instead of broadcasting your sale to the market.

- Screens buyers for fit, seriousness, and ability to transact.

- Manages negotiation so terms don't become lopsided or ambiguous.

- Coordinates diligence across finance, legal, operations, licences, and transfer requirements.

- Pushes the deal to closing when fatigue, delays, and new demands start appearing.

The founder's problem isn't usually getting initial interest. It's getting from interest to completion without chaos.

What weak brokers do differently

Weak brokers tend to behave like listing agents. They focus on exposure, not execution. You'll see some common signs:

- They ask for broad authority quickly but can't explain their buyer qualification process.

- They talk about demand in general terms instead of discussing who buys businesses like yours.

- They push for a high asking price because it wins the mandate, even if it hurts credibility later.

- They rely on mass sharing rather than controlled outreach and staged disclosure.

A broker earns their fee when the process gets messy, not when they send the first teaser.

What strong brokers sound like

A specialist broker usually talks in specifics. They'll ask how revenue is concentrated, whether licences are transferable, what key staff must stay, how customer contracts are structured, and what a buyer would need to assume operational control on day one.

That's the right conversation. In Dubai, business brokers create value by reducing deal friction. The closer they operate to the mechanics of transfer and handover, the more useful they are.

Navigating the UAE Market and Regulations

The UAE sale process gets practical very quickly. Legal structure, licensing authority, shareholder setup, and operating dependencies all shape what a buyer is acquiring.

In many parts of the UAE, including Dubai, licensing may be required to operate as a business broker, and entry often involves professional courses and exams. A UAE guide also notes that compensation is usually commission-based, according to this UAE business broker guide. For founders, that matters because it signals a more formal brokerage environment than informal introductions and handshake-only arrangements.

Mainland and free zone sales don't feel the same

Founders often talk about “selling the company” as if the route is uniform. It isn't.

A mainland business may involve one set of transfer steps and approvals. A free zone entity may involve another, with its own authority, forms, compliance process, and practical restrictions. Even before you get to legal drafting, you need clarity on what exactly changes hands and what third-party approvals sit around the transaction.

That has consequences for timing. If your broker can't explain the administrative path in your jurisdiction, they're not ready to run your deal.

For founders with entities or counterparties connected to financial free zones, public record checks can be part of basic diligence. The DIFC public register guide is a useful reminder that verification work should start early, not after a buyer has already spent weeks in review.

The local details that change outcomes

In Dubai, a sale can depend on details that generic guides skip:

- Licence continuity. Can the buyer continue operating smoothly after transfer?

- Approvals outside the SPA. Some steps sit with regulators, free zones, landlords, or banks.

- Visa and staffing dependencies. A transfer can affect practical day-to-day continuity.

- Banking handover. Even when a deal is agreed, bank-related dependencies can slow execution.

- Document quality. Missing ownership, accounting, or approval records can weaken buyer confidence.

What to ask your broker about regulation

Ask direct questions, not broad ones.

- Which authority governs my company's transfer process?

- What approvals usually delay transactions in this jurisdiction?

- What documents should I prepare before buyers enter diligence?

- How do you sequence legal, operational, and administrative workstreams?

If the answers stay generic, keep looking. In Dubai, regulatory fluency isn't a bonus skill. It's part of the core job.

A Practical Checklist for Vetting Business Brokers

Dubai doesn't have a tiny broker market dominated by a handful of firms. SMERGERS lists 80 active and verified business brokers in the city as of 9 March 2026, according to its Dubai broker directory. That fragmentation is the main reason founders need a serious screening process. You're not choosing between obvious leaders. You're sorting through very different levels of quality.

Start with capability, not charm

A polished broker meeting proves almost nothing. You need evidence that the person can run your type of transaction.

Use this checklist.

- Check specialisation first. Ask whether they primarily sell businesses, not property or mixed opportunities. You want someone whose day-to-day work is business transfers.

- Test sector familiarity. A broker who understands F&B resale may not understand a services, tech, healthcare, logistics, or industrial transaction.

- Check jurisdiction experience. Your company's licence environment matters. Ask where they've successfully closed deals.

- Review their process map. They should be able to explain each stage from teaser to completion in plain language.

- Probe confidentiality controls. Ask how they anonymise outreach, who gets the CIM, and when buyers sign NDAs.

- Inspect buyer screening discipline. They should verify buyer seriousness before introductions multiply.

- Understand who does the work. In some firms, the senior person wins the mandate and disappears.

- Ask about mandate structure. Exclusivity can make sense, but only if reporting, scope, and performance expectations are clear.

- Check how they handle diligence. Many deals slow down or break during diligence.

- Clarify communication rhythm. You need regular, decision-useful updates, not occasional optimism.

Questions worth asking in the first meeting

Don't ask, “Can you sell my business?” Ask questions that expose process quality.

- Walk me through how you'd value a business like mine.

- Who is the most likely buyer profile for this company, and why?

- How do you test buyer credibility before you bring them to me?

- What information do you share at teaser stage, NDA stage, and diligence stage?

- What usually causes deals like this to stall in Dubai?

- Which parts of my structure or licence setup might create transfer friction?

- How often will I receive updates, and what will those updates include?

- What happens if we disagree on price positioning or negotiation strategy?

- Who coordinates with lawyers and accountants during diligence?

- What does a failed process usually look like in your experience?

Founder test: If a broker can't answer these without hiding behind buzzwords, they probably won't become clearer once the process is live.

Red flags that should slow you down

Some warning signs are subtle. Others are obvious.

| Signal | What it usually means |

|---|---|

| Immediate promise of a premium price | They're selling you the mandate |

| No sharp questions about licences or ownership | They don't understand local execution risk |

| “We have many buyers” without screening detail | Weak qualification process |

| Refusal to discuss failed deals | Limited process honesty |

| Vague reporting commitments | You'll be chasing updates yourself |

A short founder scorecard

After each broker meeting, score them privately on four points:

- Process clarity

- Jurisdiction understanding

- Buyer vetting discipline

- Candour when discussing risks

That simple scorecard cuts through personality bias. Founders often hire the most confident broker. You're better off hiring the most organised one.

Broker Fees and Sale Timelines Explained

The right way to think about broker fees is simple. You're not paying for a listing. You're paying for process management, buyer screening, negotiation support, and deal completion.

In the UAE, broker compensation is typically commission-based, as noted earlier in the UAE guide. That structure can align incentives well, but only if the engagement terms are tight. Fee disputes usually start because the success conditions, tail period, exclusivity, or payment trigger weren't written clearly enough.

If you want a useful external reference on structuring the legal side of this properly, the discussion on drafting robust commission agreements is worth reading for the questions it raises around scope, trigger events, and ambiguity.

Common fee structures

| Fee Model | How It Works | Founder's Pro | Founder's Con |

|---|---|---|---|

| Success fee only | Broker is paid when the deal closes | Lower upfront cash commitment | Can attract volume-driven behaviour |

| Monthly retainer | Fixed monthly fee during the mandate | Broker has incentive to stay engaged | You pay before outcome is proven |

| Hybrid model | Smaller retainer plus closing fee | Better alignment across process and close | Terms can get messy if poorly drafted |

| Minimum fee arrangement | Broker earns no less than an agreed floor on close | Clear economics for the broker | Can feel expensive on smaller deals |

| Tiered success fee | Fee structure changes across value bands or conditions | Can align incentives around price | Harder to evaluate without examples |

What matters more than the model

Founders often fixate on percentage and ignore the contract language. That's a mistake.

Check these points carefully:

- Success definition. Is the fee triggered on signed terms, closing, or receipt of funds?

- Tail period. If a buyer introduced during the mandate returns later, what happens?

- Exclusivity scope. Are all inbound buyers covered, or only broker-introduced buyers?

- Excluded parties. List buyers already known to you.

- Expense treatment. Clarify whether marketing, travel, data room, or legal support costs sit outside the fee.

For valuation context before you even discuss fee economics, founders should also review this practical piece on startup company valuation. It helps separate valuation logic from broker salesmanship.

Timelines in the real world

Most founders underestimate how long the slow parts take. Buyer outreach can move quickly. Diligence, approvals, document cleanup, and handover planning are where time disappears.

A realistic sequence usually looks like this:

- Preparation and positioning

- Outreach and first buyer conversations

- Management discussions and indicative offers

- Diligence and legal drafting

- Approvals, transfer steps, and handover

Don't build your operating plan around the first offer. Build it around the time required to get to money in the bank and control transferred.

If you need speed, the best lever usually isn't lower price. It's cleaner documents, faster answers, and a broker who knows how to sequence the process.

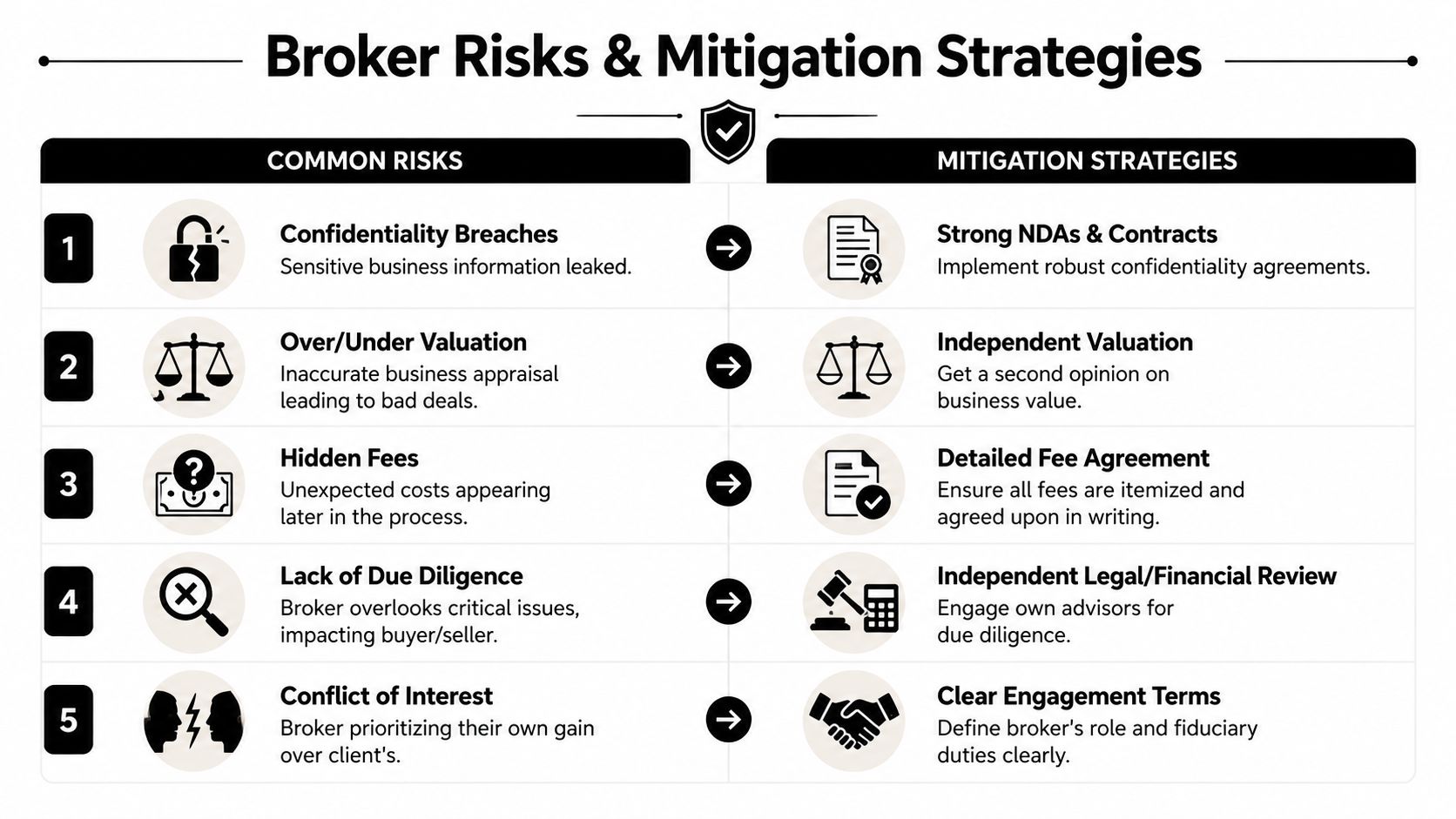

Common Risks When Using a Broker and How to Mitigate Them

The biggest misconception about brokers is that once you hire one, execution risk drops automatically. It doesn't. A weak broker can add noise, leak information, misread buyer quality, and push you into a deal structure that was shaky from the start.

One UAE-specific issue matters more than founders often expect. In a UAE-focused discussion on buying businesses, Tahir Kashif says “high street banks would not lend” and “seller financing is close to none”, with seller notes also described as uncommon in that market, in this UAE business acquisition discussion. That changes how you should judge brokers. In this market, buyer vetting isn't a courtesy step. It's one of the main filters for whether a deal can happen at all.

The risks that hurt founders most

- Confidentiality leakage. Once sensitive sale discussions spread, staff confidence and commercial relationships can wobble.

- Inflated valuation guidance. An unrealistic asking position can burn months and damage credibility with serious buyers.

- Weak buyer qualification. You spend time with people who like the idea of buying, not people who can complete.

- Hidden economics in the mandate. Ambiguous fee terms create disputes at the worst moment.

- Conflict of interest. Some brokers optimise for the fastest close, not the best fit or cleanest outcome.

How to reduce those risks

A few practical controls help immediately:

- Use staged disclosure. Anonymous teaser first, fuller information later, detailed data only after serious progress.

- Get an independent view on valuation. Even a sanity check from your accountant or adviser helps.

- Ask for buyer qualification criteria in writing. Proof of funds, acquisition rationale, decision-maker identity, and timing.

- Define mandate terms tightly. Scope, exclusivity, fee trigger, excluded parties, and reporting rhythm should all be explicit.

- Keep your own advisers involved. Broker, lawyer, and accountant should not be the same source of judgment.

Buyers don't kill most deals in Dubai. Poor qualification and weak process discipline do.

One overlooked value driver

Founders also forget that reputation can influence buyer confidence. If your company has public trust issues, disputes, or visible brand damage online, those concerns can affect deal appetite and negotiation posture. This analysis on ContentRemoval.com's valuation insights is a useful reminder that valuation isn't only about financial statements.

A broker who ignores that layer is working with an incomplete picture. A good one spots it early and helps you decide whether to fix the issue before going to market.

Your Next Steps and Alternatives to a Broker

A broker makes sense when you need structured buyer outreach, confidentiality control, negotiation support, and someone driving the process while you keep the business stable. That's especially useful if this is your first sale, your buyer universe isn't obvious, or your transfer path has real administrative complexity.

A broker may be less useful if you already have a warm strategic buyer, the transaction is highly specialised, or the business is so small and straightforward that a marketplace listing plus legal support is enough. Some founders hire a broker because they feel they should. That's not a good reason.

A simple decision framework

Use these questions:

- Do I need active buyer sourcing, or do I already know the likely buyer?

- Is confidentiality critical?

- Will jurisdiction, licences, approvals, or handover make this sale operationally tricky?

- Can I run a sale process while still operating the company properly?

- Do I need help with negotiation and diligence control, not just introductions?

If most answers are yes, a broker is probably useful. If most answers are no, consider alternatives.

The main alternatives

Specialist M&A adviser

Better for larger or more complex transactions, especially where buyer strategy, negotiation depth, and deal structuring matter more than broad market exposure.

Direct sale

Works when there's already a credible buyer in view. You'll still need legal and financial support, but you may not need a broker.

Marketplace route

Practical for simpler businesses where broad exposure is acceptable and confidentiality is less sensitive. You'll need to manage filtering carefully.

Trusted network introductions

Often underestimated. Warm introductions from founders, operators, and investors can produce higher-quality conversations than cold market outreach. If you're weighing a sale against other strategic options, this piece on UAE startup exits versus acquisitions trends helps frame how different paths can play out.

What to do this week

Keep it simple.

- Write a one-page seller brief for yourself. Why sell, why now, what outcome do you want?

- List every dependency that could affect transfer, including licences, banks, visas, key staff, and major contracts.

- Interview three brokers using the same questions.

- Ask each to explain how they'd qualify buyers in the UAE context.

- Compare them on process quality, not personality.

The best business brokers in Dubai don't just bring interest. They remove failure points. That's the standard worth hiring against.

Founder exits are easier when you can compare notes with people who've gone through them. Founder Connects gives UAE and MENA founders a high-signal network for practical conversations, curated introductions, and honest support when big decisions like a sale, acquisition, or strategic pivot are on the table.

Building in MENA? You don't have to do it alone.

Join 300+ founders in the Founder Connects Residency. Monthly squad calls, warm intros, $3M+ in perks, and much more. All for less than your monthly coffee budget.

Popular posts

The premier community for tech founders, investors, and builders. Connect, collaborate, and grow together.