A Guide: Convertible Notes vs Safe Uae Startups

Building in MENA? You don't have to do it alone.

Join 300+ founders in the Founder Connects Residency. Monthly squad calls, warm intros, $3M+ in perks, and much more. All for less than your monthly coffee budget.

You're probably in the same place most first-time founders in the UAE reach sooner than expected. You need to close a small round quickly, one investor says “just use a SAFE”, another says “I only do convertible notes”, and your lawyer starts asking which jurisdiction your company sits in and what happens at maturity.

That's not admin. It's one of the first real financing decisions that can shape your cap table, your legal exposure, and the tone of your investor relationships.

For convertible notes vs SAFE UAE startups, the wrong answer usually isn't about theory. It's about fit. A structure that works smoothly in Silicon Valley can create friction in Dubai, Abu Dhabi, or on the mainland if the investor base, legal counsel, or future round dynamics are different. The practical question is simple: which instrument helps you raise now without creating avoidable pain later?

Your First Funding Round SAFE or Convertible Note

Most founders first hear these terms in a hurry. You're trying to keep payroll moving, finish product, maybe close a few angels, and someone sends over a template. At that point, it's tempting to treat a SAFE and a convertible note as interchangeable. They aren't.

A convertible note starts life as debt. It's money invested now that usually converts into equity later, but until conversion it carries the logic of a loan. A SAFE is different. It's an agreement for future equity, not a debt obligation.

That distinction matters early.

Globally, SAFE notes were approximately five times more common than convertible notes in H1 2023, and the same source notes that founders often save roughly 1% to 2% in dilution per year of bridge financing because SAFEs don't accrue interest, unlike convertible notes that typically carry 4% to 8% annual interest and 18 to 24 month maturity deadlines. The same analysis also points out why this has been especially relevant for founders in hubs like Dubai Technology and Media Free Zone, where speed and simpler cap table modelling often matter more than debt-style investor protections. That data is discussed in Qubit Capital's breakdown of SAFE notes and convertible debt.

The practical fork in the road

If you're raising a true pre-seed or early seed round from angels, operator-investors, or accelerators, a SAFE often matches the reality on the ground better. It's cleaner, faster, and usually easier to explain to investors who are backing the team more than the spreadsheet.

If you're speaking with more traditional investors, family offices, or institutions, the conversation often changes. They may want a structure they already know how to diligence and enforce.

Fast rule: If you can't comfortably explain what happens on conversion, on delay, and on a failed next round, you shouldn't sign either document yet.

What to decide first

Before you look at templates, answer these:

- Who's investing: angels and accelerators, or institutional capital?

- How fast you need to close: days matter in small rounds.

- Where your entity sits: ADGM, DIFC, a free zone, or mainland can change the drafting and investor comfort level.

- What risk you can absorb: especially if repayment can ever become a live issue.

The Core Mechanics of Each Instrument

A lot of confusion disappears once you strip away legal vocabulary and look at each instrument for what it really is.

How a convertible note actually works

A convertible note is best understood as a short-term loan that hopes to become equity later.

An investor gives the company cash now. Instead of being repaid in the ordinary way, the note is usually designed to convert into shares when a future financing round happens. Until that trigger arrives, though, the instrument behaves like debt in key ways.

The main moving parts are usually:

- Interest: the amount owed grows over time if the note hasn't converted.

- Maturity date: there is a date when the note must convert, be repaid, or be renegotiated.

- Valuation cap or conversion price mechanics: these determine how favourably the investor converts.

- Discount: the investor may convert at a better price than later investors.

For founders, the two terms that cause most trouble are interest and maturity. Interest increases the amount that will convert. Maturity creates a hard conversation if the next round takes longer than planned.

How a SAFE actually works

A SAFE is easier to understand if you think of it as a pre-paid ticket for future shares.

The investor pays now. The company doesn't issue equity immediately. Instead, the investor gets the contractual right to receive shares later if a defined trigger happens, usually a future priced round. There's no interest running in the background, and there's usually no maturity date hanging over the company.

That changes the founder experience in a meaningful way. You're not carrying debt logic while trying to prove the business.

Common SAFE terms still matter:

- Valuation cap: this can protect the investor if your next round is priced much higher.

- Discount: this can reward the investor for coming in early.

- Conversion trigger: this tells everyone when the SAFE turns into equity.

Why founders mix them up

Both instruments delay the valuation fight. That's why they get grouped together.

But they solve the problem differently. The note says, “invest now, debt first, equity later.” The SAFE says, “invest now, equity later, no debt in between.”

If you want a broader look at how investors compare deferred financing with priced equity, this guide on convertible notes vs equity and which structure angel investors prefer is worth reading before you sign anything.

A founder usually feels the difference between these instruments only when timing slips. On paper they can look similar. In a delayed round, they don't feel similar at all.

The simplest mental model

Use this mental shortcut:

- Convertible note: loan with an equity destination.

- SAFE: future equity claim with no loan in the middle.

If you keep that distinction clear, most of the downstream trade-offs become easier to judge.

Direct Comparison for UAE Founders

Founders don't need a law school answer here. They need to know what tends to work, what creates friction, and what trade-off they're accepting.

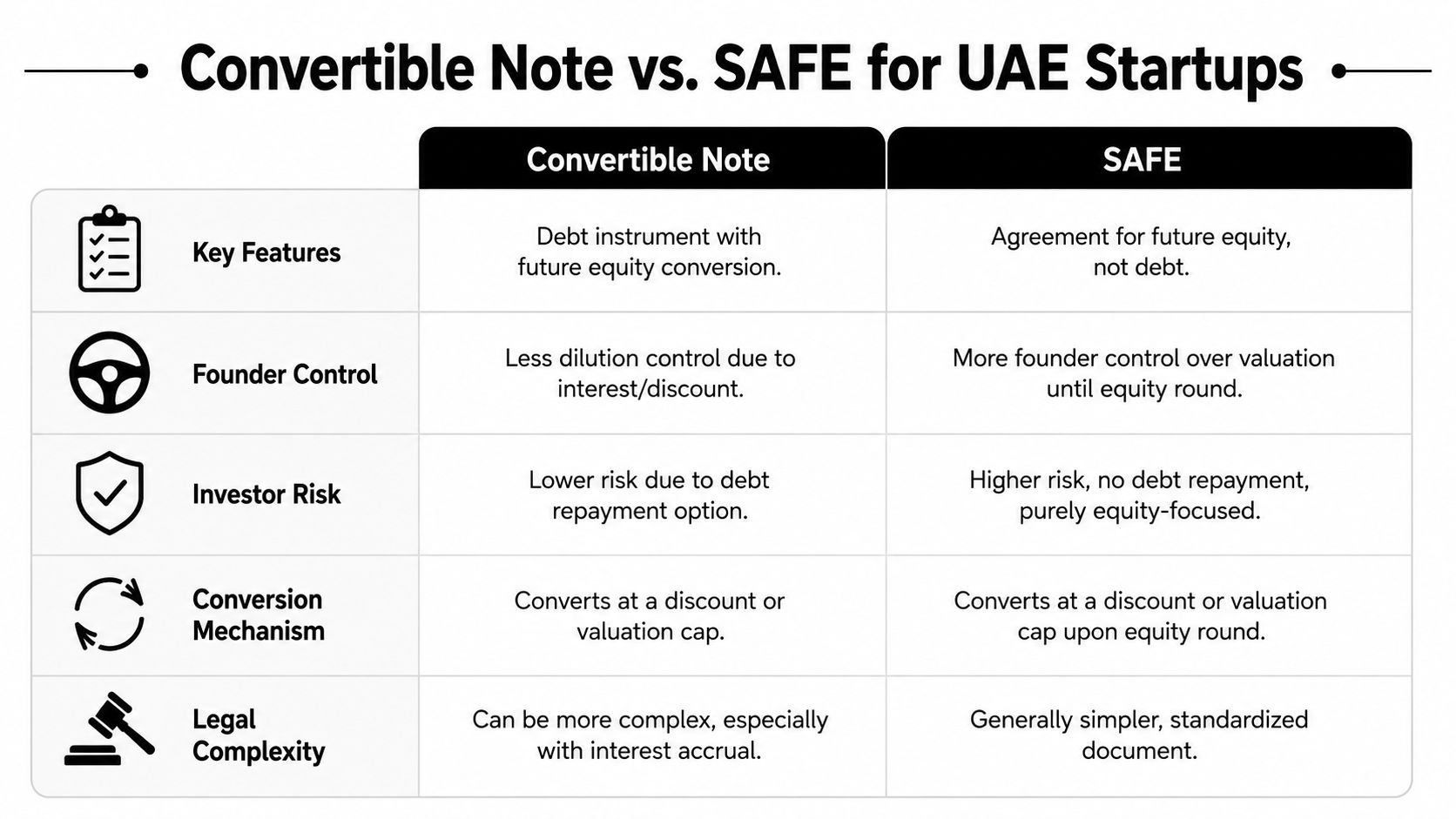

Convertible Note vs. SAFE at a Glance

| Feature | Convertible Note | SAFE (Simple Agreement for Future Equity) |

|---|---|---|

| Legal nature | Debt instrument | Future equity agreement |

| Interest | Usually includes interest | No interest |

| Maturity date | Yes, typically included | Usually no maturity date |

| Repayment pressure | Possible if conversion doesn't happen as planned | No debt repayment obligation in the same way |

| Founder simplicity | More moving parts | Simpler to document and explain |

| Investor protection | Stronger on paper because of debt structure | Lighter protection, more equity-style risk |

| Cap table impact | Can lead to extra dilution because of accrued interest | Usually cleaner to model |

| Best fit | When investor insists on debt-style familiarity | When speed and founder flexibility matter most |

If you're comparing convertible notes vs SAFE UAE startups, this is the quick answer: SAFEs are usually better for speed and founder flexibility, notes are usually better for investor protection and legal familiarity.

Founder friendliness

For most early-stage founders, SAFEs are more forgiving.

There's no interest ticking upward, and there's usually no maturity date forcing a decision before the company is ready. That doesn't make SAFEs “better” in every case, but it does make them easier to live with when the business is still fragile.

Key differentiator: A SAFE removes the debt clock. A convertible note keeps it running.

Convertible notes can still be founder-friendly if the investor is sensible and the terms are light. But the baseline structure isn't founder-first. It's a debt instrument designed to convert later.

Investor friendliness

Notes often prove more favorable.

An investor who wants stronger downside protection will usually feel better holding a note than a SAFE. The note gives them a more conventional legal position while they wait for conversion. In practical fundraising conversations, that often matters most with investors who come from private credit, family office, or traditional corporate backgrounds.

SAFEs ask the investor to accept more uncertainty. Some angels are perfectly comfortable with that. Some aren't.

Legal complexity and paperwork

A SAFE usually closes faster. Fewer moving parts means fewer negotiation points.

Convertible notes tend to create longer redlines because you're not only discussing future conversion. You're also dealing with debt terms. Interest, maturity, default-style language, and what happens if the company misses expectations all increase drafting complexity.

For a founder trying to close a modest bridge or pre-seed round, that difference can be decisive.

Repayment risk

This is the issue many first-time founders underestimate.

With a convertible note, if the next round doesn't happen on time and the maturity date arrives, the investor may have repayment rights or a strong position in the renegotiation. That can become a real business problem at the worst possible moment.

With a SAFE, that debt-style repayment risk isn't the same issue because there's no maturity date in the ordinary structure.

If you're still searching for product-market fit, avoid instruments that punish delay unless you have a very clear reason to accept that risk.

Cap table maths

Founders often focus on valuation cap and discount, then ignore the impact of interest.

That's a mistake. With a convertible note, interest can increase the amount converting into equity, which can lead to more dilution than expected. With a SAFE, there's no accrued interest adding to the conversion base, so the cap table is usually easier to model and explain.

This matters even more when you've raised from multiple small cheques. The more moving pieces you stack, the more a “simple bridge” can become messy by the next priced round.

What usually works in practice

Here's the practical reading:

- Use a SAFE when you're raising from angels, operators, or pre-seed backers who care about speed and don't need debt-style protections.

- Use a convertible note when the investor insists on a debt instrument, or when legal familiarity matters more than founder simplicity.

- Don't use either casually if your company structure is already messy or your next round timeline is highly uncertain.

If you're preparing for those investor conversations, this guide on fundraising for startups helps frame the broader process around instrument choice.

Investor Preferences and Legal Quirks in the MENA Region

A lot of generic startup content misses the point here. In the UAE and MENA, the instrument isn't judged only on economics. It's judged on legal comfort, drafting standards, and whether the investor has seen the structure work locally before.

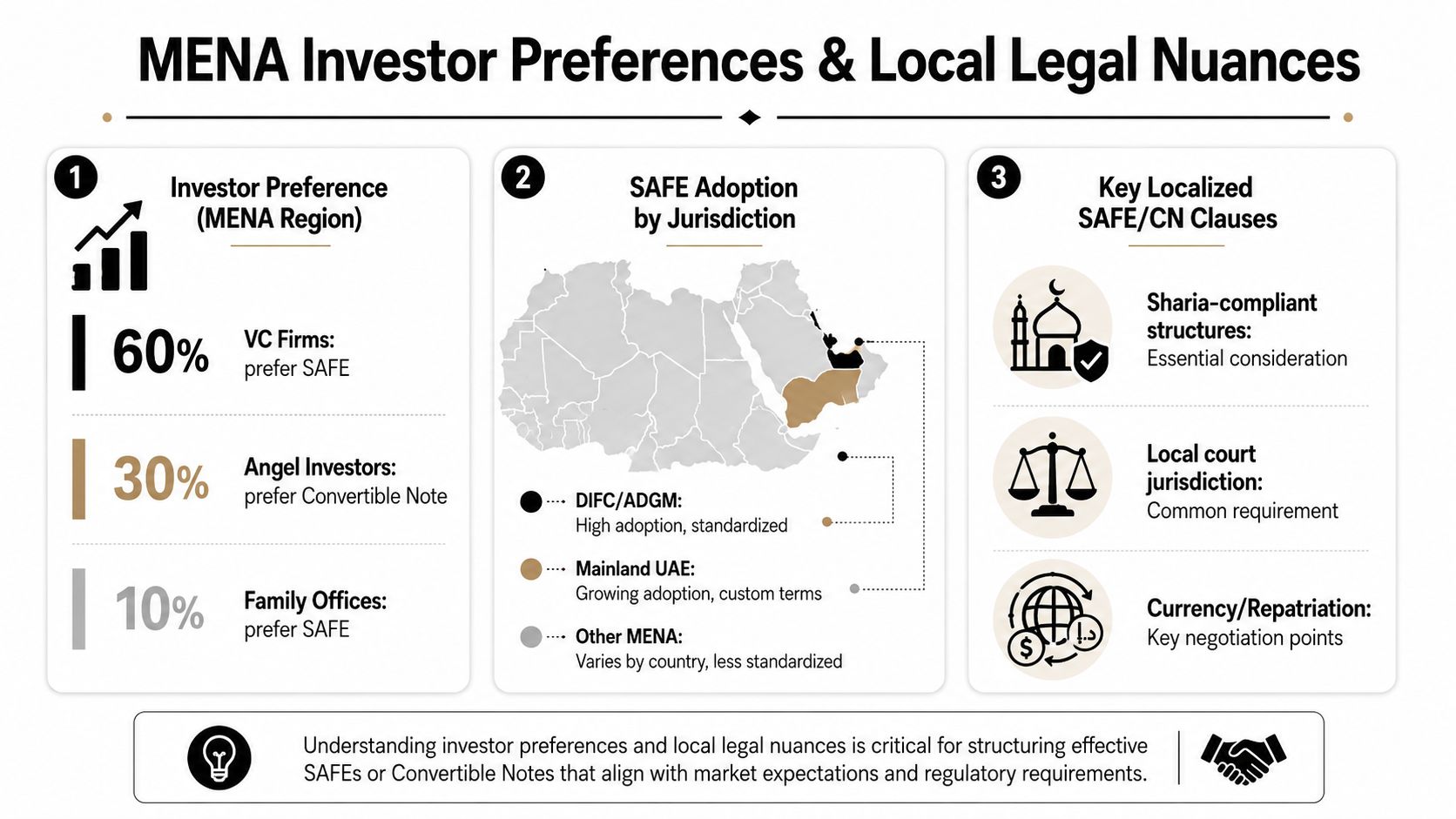

What early-stage investors are actually doing

In the UAE and broader MENA pre-seed market, 90% of deals conducted in Q1 2025 used SAFEs, driven by their zero-interest structure and lack of maturity dates, especially for startups raising $50K to $500K from angels. That detail appears in CRV's discussion of SAFEs vs convertible notes.

That lines up with what many founders see on the ground. Small angel rounds need to close quickly. Investors don't want a full priced equity round. Founders don't want debt pressure before the company has even settled its operating rhythm.

Why the legal context still matters

ADGM and DIFC are usually more comfortable environments for modern startup financing documents because founders, investors, and counsel there are used to more flexible deal structures. A SAFE can feel natural in that setting, especially when the investor already understands YC-style documents.

Mainland and non-financial free zone situations can be less straightforward. The issue isn't that SAFEs can't be done. The issue is that local implementation, future conversion mechanics, and investor comfort may require more tailoring.

That's where first-time founders get caught. They assume a US template will travel cleanly. Sometimes it does. Sometimes it absolutely doesn't.

What more traditional investors often prefer

Institutional funds, some family offices, and more conservative legal teams in the region often lean toward structures they can diligence with less interpretive friction.

That doesn't automatically mean they reject SAFEs. It means they may ask harder questions about enforceability, conversion language, governing law, and what happens if the next round never arrives.

A SAFE in the abstract is simple. A SAFE across the wrong jurisdiction, with the wrong investor, and unclear local drafting is not simple at all.

Practical UAE checklist before you circulate a document

- Check entity jurisdiction: ADGM, DIFC, mainland, and some free zones can produce different drafting realities.

- Ask what paper the investor already uses: many delays happen because each side assumes its own template is “standard”.

- Confirm governing law early: don't leave this until the final mark-up.

- Map the next round path: if later institutional money is likely, ask current counsel how today's document will look in due diligence.

If you're preparing to speak with local angel investors, this guide on how to pitch UAE angel investors is useful alongside the instrument decision because the two conversations usually happen together.

A Founder's Regret The Wrong Choice in Dubai

A real cautionary story captures the risk better than any model.

A UAE founder raised $300,000 on a convertible note with a 2-year maturity and 6% interest. At the time, the choice probably felt reasonable. The founder got capital in, delayed the pricing discussion, and kept the round moving.

Then the next round took longer than planned.

The company didn't raise its Series A before the note matured. Once the maturity date hit, the debt logic stopped being background paperwork and became the central problem. The company faced a mandatory repayment obligation it couldn't meet, and the note terms led toward a forced liquidation clause. That scenario is described in Finvisor's discussion of pre-SAFE, post-SAFE, and convertible notes.

Why this went wrong

The mistake wasn't just “using a note”.

The mistake was using a note when the company's future fundraising timeline was uncertain and the downside of delay was severe. Early-stage founders often build their financing assumptions around the best-case version of the next twelve to twenty-four months. The legal document, however, applies to the actual version.

That's where maturity dates become dangerous. They turn fundraising delay into a legal advantage.

The lesson most founders should take

If you're still proving distribution, still tightening the product, or still relying on a small group of angels, no repayment risk should be high on your priority list. Unless an institutional investor explicitly requires a debt instrument, a SAFE usually gives a younger company more breathing room.

The problem with a maturity date isn't the date itself. It's what happens when the company reaches that date before the market cooperates.

For first-time founders in Dubai, this is the practical takeaway. Don't choose the instrument that sounds more complex. Choose the one your business can survive if fundraising takes longer than you hoped.

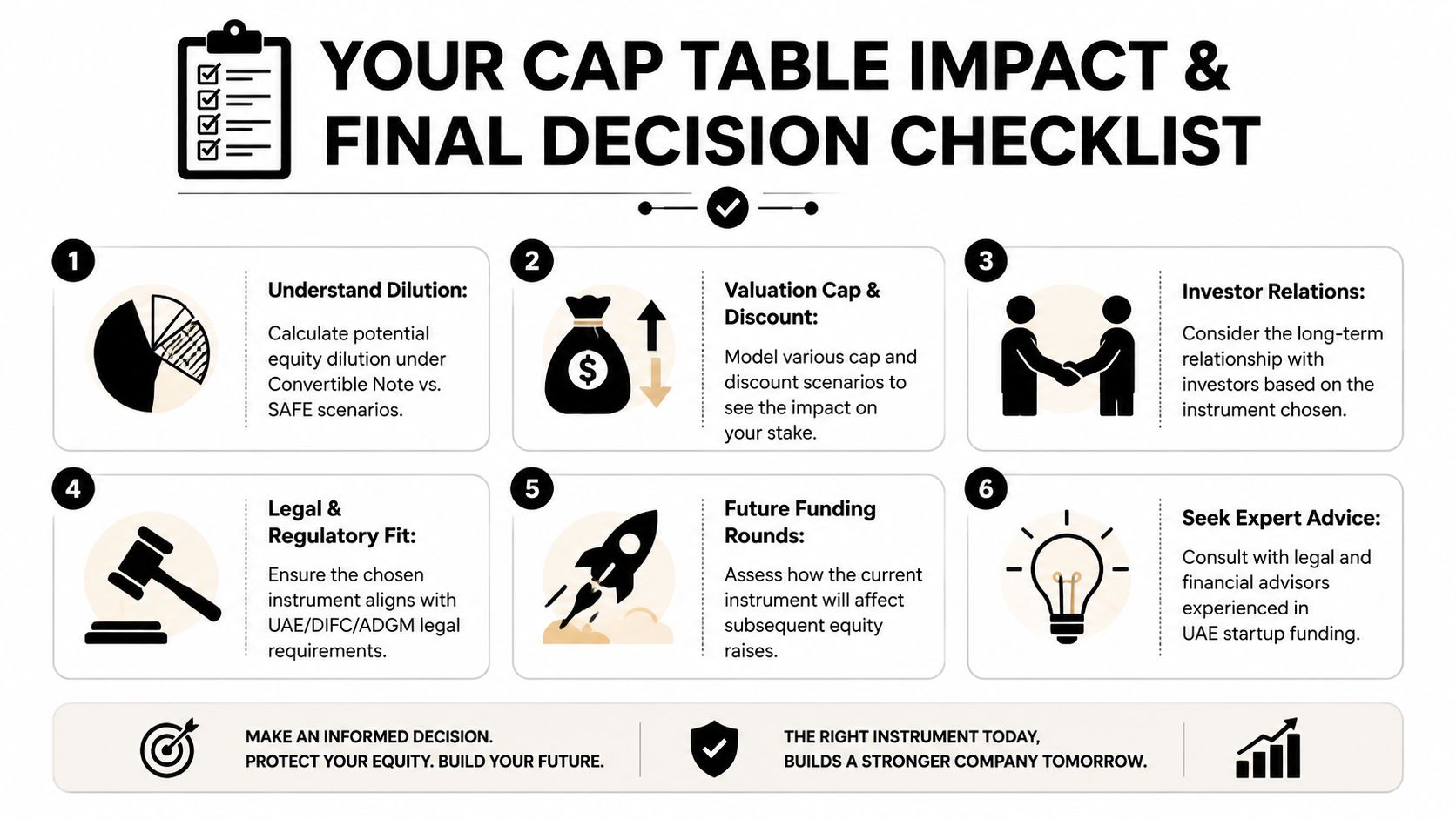

The Cap Table Impact and Your Final Decision

Founders usually feel financing pain in two places. One is legal stress. The other is dilution they didn't properly model.

Where cap table surprises come from

With a SAFE, your conversion maths is usually easier to explain because there's no interest accumulating before conversion. You still need to model the valuation cap, any discount, and the effect of multiple SAFEs stacking on top of each other, but the basic logic is cleaner.

With a convertible note, the conversion amount may be larger because the principal can increase through accrued interest before the note turns into equity. Founders often miss that in early discussions because everyone focuses on the headline cash invested, not the amount that may convert later.

That's why notes can produce more dilution than a founder intuitively expects, even when the initial cheque size looked manageable.

Why local legal preference affects the decision

In the UAE and wider MENA region, institutional investors and law firms often prefer convertible notes because debt is more legally familiar and easier to enforce under local contract law than the US-specific SAFE structure. That familiarity can reduce diligence friction because courts and counsel are more accustomed to debt repayment and maturity concepts than the grey-zone equity classification of SAFEs. That point is outlined in Lazo's analysis of SAFEs and convertible notes.

That doesn't mean you should default to a note. It means the “best” instrument depends on who needs comfort in the transaction.

A simple decision framework

Use these questions before you sign:

Who is this round for

- If it's angels and accelerators, a SAFE often fits.

- If it's institutional capital, ask whether they already expect note-style paper.

How certain is your next priced round

- If timing is unclear, debt with maturity can become a problem.

- If the next round is highly likely and already warming up, a note may be manageable.

How much negotiation bandwidth do you have

- A SAFE often closes faster.

- A note can consume more founder and legal time.

What will future investors think

- Ask counsel how this instrument will look in your next diligence room.

- Don't optimise for today if it creates avoidable friction later.

Can you model the dilution clearly

- Run the conversion assumptions before signing.

- If you can't explain the cap table impact in plain English, pause.

Decision rule: If speed, simplicity, and no repayment risk matter most, start with a SAFE. If investor familiarity, debt-style protections, and legal conservatism drive the round, a convertible note may be the right compromise.

The version I'd use and why

For a true UAE pre-seed round, I'd usually choose a SAFE. The reason is straightforward. Most first rounds need flexibility more than debt mechanics. Founders need to close capital, keep the cap table readable, and avoid a maturity problem while the business is still proving itself.

I'd switch to a convertible note only when the investor mix makes that necessary, especially if a more institutional lead or their counsel won't get comfortable with a SAFE under the company's chosen jurisdiction.

Your next action is simple. Take your current draft, ask your lawyer to model the conversion outcome and downside case, then ask one blunt question: what happens if our next priced round is late? If the answer makes you uneasy, don't sign yet.

Founders make better funding decisions when they can compare notes with people who've been through them. Founder Connects brings UAE and MENA founders into curated peer groups, practical conversations, and high-signal introductions so you can pressure-test choices like SAFEs, notes, investor fit, and fundraising timing before they become expensive mistakes.

Building in MENA? You don't have to do it alone.

Join 300+ founders in the Founder Connects Residency. Monthly squad calls, warm intros, $3M+ in perks, and much more. All for less than your monthly coffee budget.

Popular posts

The premier community for tech founders, investors, and builders. Connect, collaborate, and grow together.