Revenue Based Financing for Startups UAE: Your 2026 Guide

Building in MENA? You don't have to do it alone.

Join 300+ founders in the Founder Connects Residency. Monthly squad calls, warm intros, $3M+ in perks, and much more. All for less than your monthly coffee budget.

A founder I know in Dubai ran a strong direct-to-consumer brand and needed working capital ahead of a major seasonal sales push. She could have raised equity, but giving up a meaningful slice of the company for inventory and paid acquisition felt like the wrong trade, so she chose revenue based financing instead.

Funding Growth Without Selling Your Company

Fatima had the kind of problem most founders want. Customers were buying, repeat orders were coming in, and marketing channels were already producing sales she could model with reasonable confidence. What she lacked was cash at the exact moment cash mattered most, right before a high-demand retail window.

An equity round would have solved the short-term need, but it came with two costs founders often underestimate. First, dilution for something operational rather than for strategic growth. Second, time. A seed process can drag management attention away from the thing that creates value, which is running the business.

That is where revenue based financing for startups in the UAE starts to make sense. It sits inside the broader world of non-dilutive funding for startups, but it's far more specific than a generic “keep your equity” option. It works best when the capital use case is clear, revenue already exists, and the founder wants growth money without adding a new shareholder to the cap table.

Why Fatima chose RBF

Her decision was simple once she framed the use of funds properly:

- Inventory was the main need: She wasn't funding open-ended research or a long product build.

- Demand already existed: She had real sales history, not a story built on projections.

- Marketing spend was trackable: She knew which channels worked and where extra spend would go.

- Control mattered: She didn't want investor approvals, board pressure, or an early valuation setting the tone for future rounds.

Practical rule: If the money is going into something repeatable and revenue-linked, RBF deserves a serious look.

This is also why I tell founders not to group all capital together. “Money is money” is lazy thinking. The right funding type depends on what the money is for. If you're financing a known engine, RBF can be clean. If you're financing uncertainty, it usually isn't.

For founders weighing options, it also helps to compare RBF against other local routes before you commit. This overview of funding sources for UAE tech startups is useful because it forces the right question. Not “can I raise?”, but “what type of capital matches this stage and this problem?”

RBF is not cheap money. It is not founder-friendly by default. But in the right case, it can be much smarter than selling equity too early for needs that should never have gone onto your cap table in the first place.

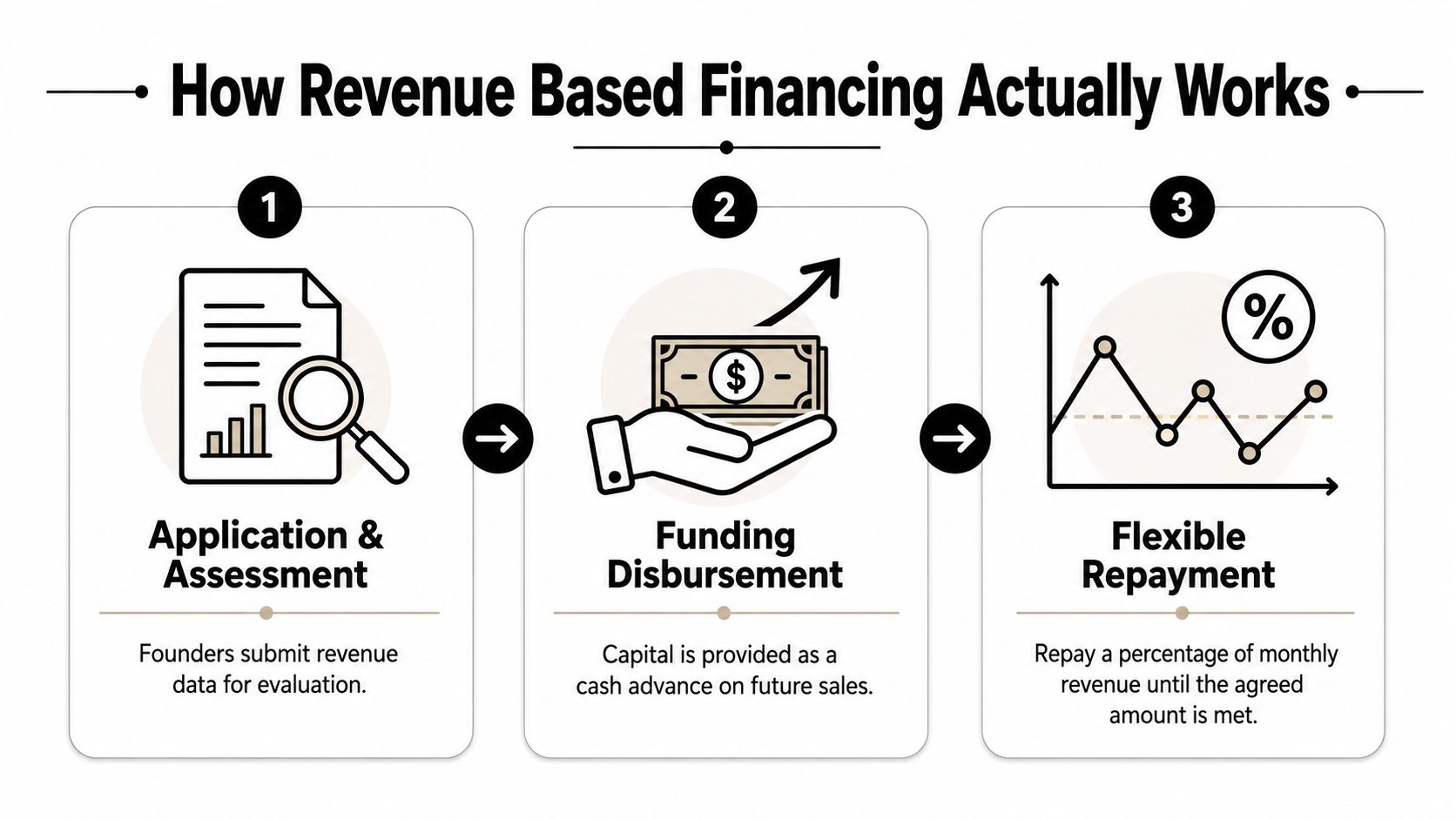

How Revenue Based Financing Actually Works

Think of RBF as a cash advance against future revenue. A provider gives your startup capital now, then takes an agreed share of your monthly revenue until a fixed repayment amount is met. You keep your equity, but you commit part of future cash flow.

That structure matters because repayment flexes with performance. Strong month, you pay more. Slower month, you pay less. That's what makes RBF feel more founder-friendly than rigid debt for businesses with uneven monthly sales.

The three moving parts

Most RBF deals come down to three practical terms:

| Term | What it means | Why it matters |

|---|---|---|

| Capital amount | The upfront funding you receive | Determines what you can actually finance |

| Revenue share | The portion of monthly revenue paid to the provider | Affects cash flow pressure each month |

| Repayment cap | The total amount you repay before the agreement ends | Defines the full cost of capital |

If you can explain those three items to your co-founder in plain English, you understand the model.

What the repayment experience feels like

Here's the part many founders miss. RBF is not judged only by the headline offer. It's judged by how repayment behaves during an ordinary operating month in your business.

A good fit looks like this:

- You can still pay suppliers comfortably

- Marketing doesn't stall because of the revenue share

- Payroll stays insulated from repayment stress

- Your margin profile leaves room for the provider's cut

A bad fit looks like this:

- Every strong month creates a cash squeeze

- Repayments interrupt inventory cycles

- You start using expensive short-term fixes to cover normal operations

- The facility helps growth at first, then chokes it

If the repayment flow only works in your best-case month, the facility doesn't work.

For subscription businesses, recurring revenue quality matters more than founders often realise. If you want a useful plain-English refresher on what stable recurring revenue really means, Fundl's recurring revenue guide is worth reading before you speak with any provider.

How providers assess the risk

In practice, providers usually want direct visibility into your revenue systems. They may review payment processor data, bank statements, ad account performance, accounting software, and cohort behaviour if you run SaaS or subscriptions.

That's why RBF often feels operationally lighter than an equity round but more data-heavy than founders expect. You won't spend months telling a big vision story. You will spend time proving your revenue is real, repeatable, and visible.

If you want a sharper breakdown of where RBF sits between debt and venture capital, this explainer on revenue-based financing as debt-like growth capital captures the strategic framing well.

The right way to think about RBF is simple. It is not fuel for invention. It is fuel for a machine that already works.

Who Qualifies for RBF in the UAE

In the UAE, providers usually care less about your pitch deck and more about whether they can verify commercial performance quickly. They want businesses with visible revenue, clean financial records, and a business model that turns growth spend into sales without too much delay.

That immediately rules some founders in and some founders out.

The practical qualification checklist

If you're asking whether revenue based financing for startups UAE is realistic for your company, start here:

- Live revenue already exists: Providers want operating businesses, not pre-launch plans.

- Revenue history is consistent: A few random spikes won't help if the base business is unstable.

- Digital transaction trails are clean: Stripe, Telr, Checkout.com, Shopify, app store dashboards, and similar systems make underwriting easier.

- Accounts are organised: Xero, Zoho Books, QuickBooks, and properly reconciled bank statements reduce friction.

- Gross margins are healthy enough: If margins are too thin, the revenue share becomes painful fast.

- Use of funds is specific: Inventory, paid acquisition, or expansion into a proven channel is easier to finance than broad “growth”.

- Founders understand their unit economics: If you can't explain CAC, payback logic, repeat purchase behaviour, or contribution margin, you're not ready.

Business models providers usually like

RBF works best when sales are trackable and repeatable. In the UAE market, these models tend to fit well:

| Business type | Why it often fits |

|---|---|

| SaaS | Subscription revenue is easier to assess if churn is under control |

| E-commerce | Inventory and paid media can often be tied directly to revenue outcomes |

| Consumer apps | Good fit when monetisation is active and performance data is reliable |

| Marketplaces with strong take rates | Can work if transaction volumes are established |

A founder with a Shopify store, Meta ad history, and clean payment data often gets evaluated faster than a founder with strong storytelling but weak reporting discipline.

Founder check: Open your accounting stack and payment dashboards before you apply. If your data is messy, fix that first.

UAE-specific realities that matter

Local context matters more than most generic RBF articles admit. If your startup operates through a UAE free zone or mainland entity, keep your commercial paperwork clean and current. Providers may also care about where revenue is booked, how collections happen, and whether the entity receiving funds matches the operating company they're assessing.

Another issue is fragmentation. Some UAE startups collect through multiple gateways, bank accounts, marketplaces, and WhatsApp-based sales flows. That may work operationally, but it makes underwriting harder. A provider wants one coherent revenue picture.

The strongest applicants are not always the fastest-growing startups. They are often the most legible startups. Revenue is visible. Reporting is current. Cash conversion is understandable. The founder answers questions directly.

If that doesn't sound like your company yet, the next action is obvious. Clean your books, consolidate your revenue reporting, and map exactly how cash moves from sale to bank account before starting any RBF conversations.

Key RBF Providers for UAE and MENA Startups

Founders don't need a giant list. They need a short list with context. The key question isn't “who offers capital?” It's “who understands my business model and underwrites the thing I'm trying to finance?”

In MENA, a few names come up regularly when founders discuss non-dilutive growth capital. They don't all look identical, and that matters.

FlapKap

FlapKap is the name many e-commerce and digital-first founders in the region encounter first. It's generally associated with businesses that need working capital tied to inventory cycles, marketing spend, and everyday growth execution.

What tends to fit FlapKap well:

- Brands selling online with established order flow

- Businesses running paid acquisition with measurable return

- Operators who need fast capital decisions tied to trading data

Where founders go wrong is applying before the business is under control. If retention is weak, return rates are messy, or ad spend efficiency moves around wildly, capital can magnify the underlying problem rather than solve it.

Erad

Erad is widely recognised in the region as a revenue-based financing player focused on non-dilutive funding for operating businesses. It usually enters the conversation for founders who already have transaction history and want capital without stepping into a traditional equity process.

Erad tends to make sense when:

| Good fit signal | Why it matters |

|---|---|

| Digital revenue is already flowing | Underwriting depends on visible performance |

| Growth use case is clear | Providers prefer defined uses over vague runway extension |

| Founder wants to avoid dilution | RBF is often chosen to protect ownership before a later round |

For UAE founders, the useful question isn't whether Erad is “better” than another provider. It's whether your company matches the type of business they can underwrite confidently.

Embedded and adjacent options

Some founders also explore adjacent products that don't market themselves purely as classic RBF but function similarly in practice. These can include merchant cash advances, invoice-linked capital, inventory finance, or embedded funding products tied to payments and commerce platforms.

That's where caution matters. Similar language doesn't mean similar economics. One product may flex with revenue in a manageable way. Another may behave much more like hard debt under the hood.

Good providers finance momentum. Bad facilities finance denial.

How to evaluate a provider properly

Don't choose based on speed alone. Use this shortlist of questions in your first call:

- What data connections do they require?

- How is repayment calculated in practice?

- What happens in a weak trading month?

- Are there restrictions on using the capital?

- Do they work well with your business model specifically?

- Will this facility limit a future equity round or bank relationship?

The next action here is practical. Build a one-page lender brief before outreach. Include your revenue trend, business model, margin profile, use of funds, sales channels, and software stack. Providers move faster when founders package the business clearly.

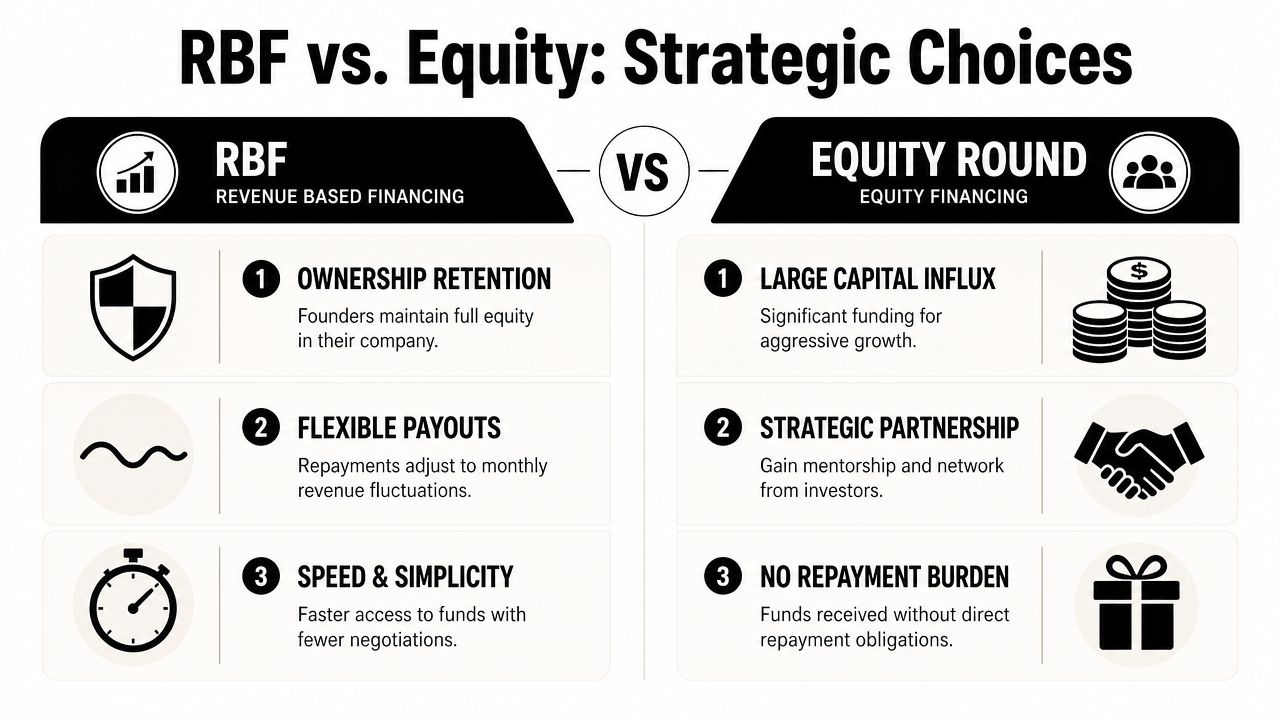

When to Choose RBF Over an Equity Round

Founders usually ask the wrong question. They ask whether RBF is better than equity. That's too broad. The right question is what kind of problem are you solving with this capital?

If the money is going into a predictable growth engine, RBF can be the sharper tool. If the money is funding uncertainty, equity is usually safer.

Choose RBF when growth is already working

RBF beats equity in a narrow but important set of situations. The classic example is a startup that has already found a repeatable channel and now wants more fuel, not a new strategy.

Pick RBF when these conditions are true:

- You know where the money is going: Inventory, paid acquisition, expansion of a proven offer, or bridging receivables.

- You can measure return with confidence: Not perfectly, but well enough to avoid guesswork.

- You care about retaining ownership: Especially if you think an equity round later will happen at a much stronger valuation.

- You need speed: A lender can often make a decision faster than a full equity process.

- You don't need strategic investor involvement yet: Some businesses need cash more than cap table complexity.

Choose equity when the company still needs belief capital

Equity is better when the business needs patient capital, strategic support, or room to make mistakes without monthly repayment pressure.

That includes cases where:

| Situation | Better fit |

|---|---|

| Product still needs major iteration | Equity |

| Market needs education before sales become repeatable | Equity |

| Regulatory or technical milestones come before revenue | Equity |

| You need investor network, signalling, or hiring support | Equity |

| Growth requires a large upfront bet beyond current cash flow | Equity |

A good investor can bring more than money. They can help with hiring, introductions, governance, and downstream fundraising. RBF doesn't do that. It's capital, not partnership.

Here's a useful general discussion on fundraising for startups if you're deciding where debt-like products fit in a broader capital strategy.

A simple decision filter

Use this three-part filter before you decide:

Is the spend reversible?

If the experiment fails, can you stop quickly and preserve the company?Is the return cycle short enough?

If cash goes out now, does revenue come back soon enough to support repayment?Would dilution here feel wasteful later?

If you're giving up equity for something operational and temporary, that should bother you.

This short video is also a useful prompt if you're weighing founder trade-offs around financing:

What works and what doesn't

What works is using RBF to scale something already validated. What doesn't work is using it to rescue weak economics, cover structural losses, or avoid making hard operating decisions.

Founders also underestimate the psychological side. Equity repayments are invisible month to month because there aren't any. RBF is very visible. You'll feel it in collections, cash planning, and monthly reporting. Some teams handle that well. Others hate it.

The best RBF users are disciplined operators. The worst are optimistic founders trying to borrow their way out of an unproven model.

My own view is straightforward. If your startup already knows how to turn capital into revenue and you want to preserve ownership, RBF can be excellent. If you still need time to discover the model, equity is usually the cleaner answer.

The One Type of Startup That Should Avoid RBF

If I had to give one hard rule, it's this. Pre-revenue, deep-tech, and R&D-heavy startups should stay away from RBF.

Not “probably”. Not “unless terms are amazing”. Stay away.

These companies have the wrong cash flow shape for revenue based financing. They need time before commercial output becomes steady enough to support repayment. Their biggest risk is not dilution. Their biggest risk is running out of time before the product, approval path, or technical milestone is ready.

Why the model breaks

RBF assumes future revenue is near enough, visible enough, and stable enough to finance against. Deep-tech and research-heavy startups usually can't make that promise.

Common danger signs include:

- Long product development cycles: Revenue may be far away.

- Regulatory dependency: Approval timing can slip without warning.

- Heavy technical burn: Cash goes into development long before it creates collections.

- Unclear commercial timing: Even good technology can take time to find a repeatable market.

That creates a bad loop. The company takes funding. Repayment pressure arrives. Revenue isn't ready. Management shifts attention from building the right product to finding short-term cash. Then quality drops, hiring gets distorted, and the capital structure starts driving the company instead of supporting it.

The death spiral founders don't see early enough

This is how the mismatch usually unfolds in practice:

| Early stage belief | What happens later |

|---|---|

| “We'll be selling soon” | Product or approvals take longer than planned |

| “We only need bridge capital” | Bridge turns into operating stress |

| “Repayments will be manageable” | Cash obligations arrive before revenue quality does |

| “This helps us avoid dilution” | The startup becomes weaker and raises equity later from a worse position |

For this category of company, equity is not the enemy. Patient capital is the product you need.

If your startup still depends on technical proof, regulatory progress, or a long runway to first meaningful revenue, repayment-linked funding is usually a self-inflicted problem.

The next action is brutally simple. Critically audit your revenue predictability. Not your hope. Not your forecast. Your actual ability to generate dependable cash in the near term. If that answer is weak, don't apply for RBF. Fix the business or pursue a better-matched capital source.

If you want sharper founder-to-founder judgement on funding choices, cap table trade-offs, and who to speak with next in the UAE ecosystem, Founder Connects is built for exactly that. It's a practical community for founders who want honest conversations, relevant introductions, and better decisions before they take on the wrong kind of capital.

Building in MENA? You don't have to do it alone.

Join 300+ founders in the Founder Connects Residency. Monthly squad calls, warm intros, $3M+ in perks, and much more. All for less than your monthly coffee budget.

Popular posts

The premier community for tech founders, investors, and builders. Connect, collaborate, and grow together.