Venture Capital vs Private Equity UAE Founders

Building in MENA? You don't have to do it alone.

Join 300+ founders in the Founder Connects Residency. Monthly squad calls, warm intros, $3M+ in perks, and much more. All for less than your monthly coffee budget.

A lot of UAE founders hit the same moment at roughly the same time. Revenue is moving, the team is stretched, someone tells you to “go raise VC”, someone else says “you're a PE story”, and both sound confident.

That advice can wreck a good business if you follow it too casually.

Capital is never just capital. It changes your board, your hiring pace, your risk tolerance, your reporting rhythm, and often your life for the next few years. In the UAE and wider MENA market, that choice is even more specific because the local funding ecosystem rewards certain business types far more than others.

The Funding Crossroads Every UAE Founder Faces

If you're building in the UAE, the confusion usually starts once the business stops looking like an idea and starts looking real. You've got customer demand, some traction, and enough proof that outside capital could speed things up. That's when the noise begins.

A fintech founder gets told to chase venture because Dubai is where startup capital sits. A profitable operator in F&B, healthcare, services, or distribution gets pushed into investor meetings that don't match how the business works. Then founders lose weeks talking to the wrong people.

The cleaner way to think about it is this. Venture capital and private equity are not two versions of the same cheque. They are two different operating philosophies.

One says: grow fast, take market share, accept more risk, and build for outsized upside.

The other says: buy or back an already proven machine, tighten it, professionalise it, and create value through execution and control.

That's why the right question isn't “who will fund me?” It's “what kind of company am I building, and what kind of investor can live with that reality?”

If you're still shaping your fundraising plan, this guide on fundraising for startups is a useful companion before you start sending decks.

The fast filter

Use this quick test before you read another investor list:

- If your company needs speed: You may fit venture capital better.

- If your company already works and needs structured expansion: You may fit private equity better.

- If your biggest concern is keeping control: You need to pay special attention to investor structure, not just valuation.

- If your ambition is personal as much as financial: Your own temperament matters as much as the company's metrics.

The biggest founder mistake here isn't picking the “wrong” capital. It's taking money from an investor whose definition of success doesn't match your own.

Understanding The Two Funding Philosophies

Before comparing term sheets, get the philosophy right.

Venture capital is creation capital

VC backs companies that are still creating the future version of their market. Product may still be maturing. Unit economics may still be evolving. The core bet is that if this works, it works at a very large scale.

In the UAE, that model has deep local relevance. Dubai hosts 90% of the country's scale-ups, Shorooq Partners has deployed $200 million into tech companies, and the market includes over 35 active investors according to Invest in Dubai's overview of venture capital and private equity. That's why founders building SaaS, fintech, AI, logistics tech, and marketplace models often find more natural conversations in venture than in private equity.

VC is rocket fuel. It's useful when your company can absorb speed.

Private equity is optimisation capital

PE usually enters once the business is no longer proving whether it works. It already works. Customers pay. Operations exist. Management reporting matters. Margins matter. Governance matters.

That investor is not asking, “Could this become huge if everything goes right?” They're asking, “How do we make this asset stronger, more valuable, and more efficient?”

For founders, that distinction matters more than jargon. If your business is an established operator with repeatable performance, PE may be a better fit than forcing a venture story onto a company that isn't built for hyper-growth. It also changes how you think about small business valuations, because PE buyers care a lot about durability, control, and operational quality rather than just headline growth.

The wrong match creates pain fast

When founders take VC for a business that really wants steady expansion, they often inherit pressure that the company can't satisfy. When they approach PE too early, they get told to come back once the business is larger, cleaner, and more institutional.

A useful rule is simple:

- Choose VC if uncertainty is still high but upside is massive.

- Choose PE if uncertainty is lower and value creation will come from disciplined execution.

- Avoid both if you're raising just because everyone around you is raising.

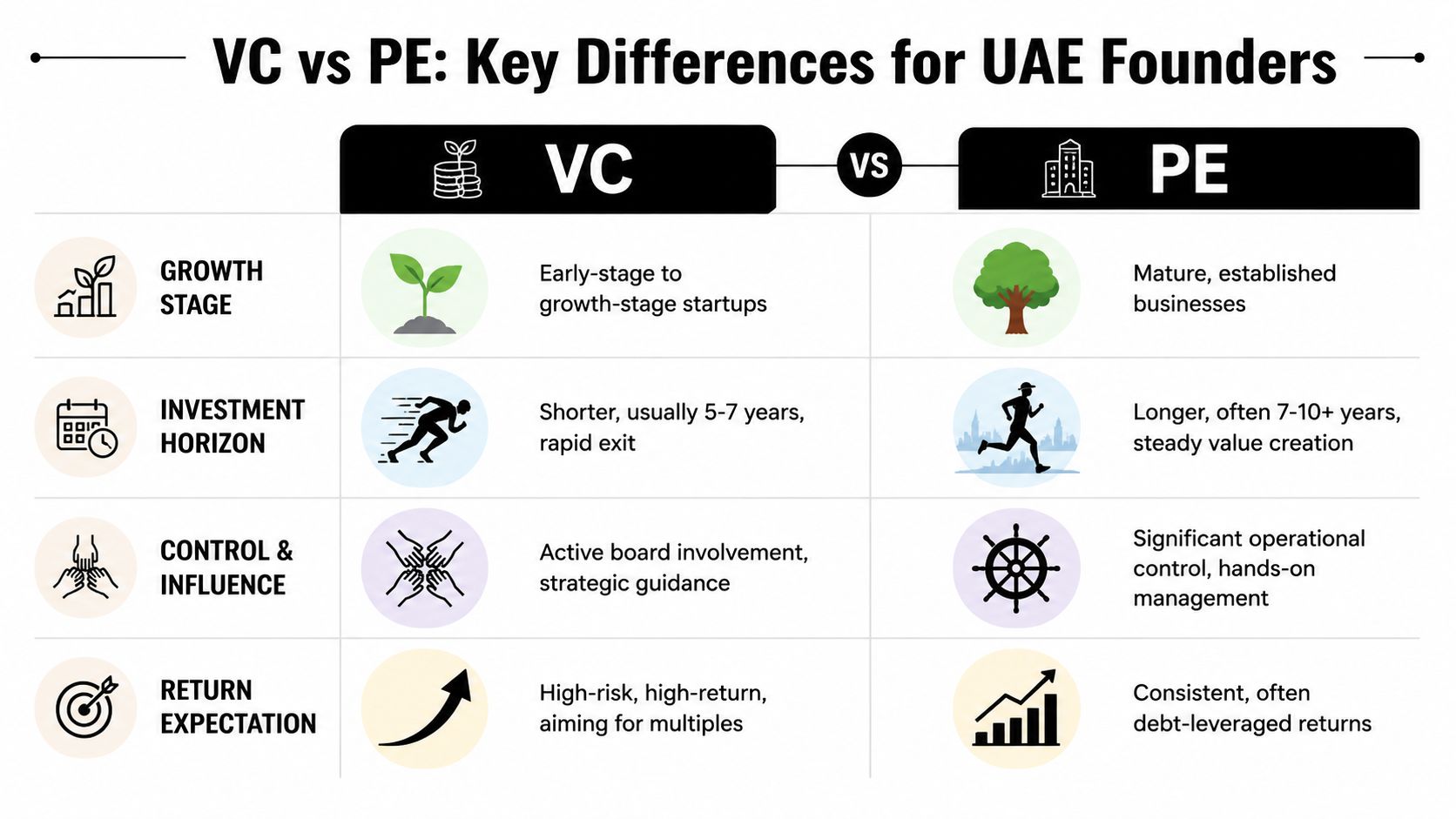

VC vs PE Core Differences for Founders

A lot of UAE founders treat this choice like a valuation exercise. It rarely is. The key decision is what kind of company you want to build, what kind of investor you want in the room, and what kind of founder you are when growth gets messy.

Venture Capital vs. Private Equity at a Glance

| Criterion | Venture Capital (VC) | Private Equity (PE) |

|---|---|---|

| Growth stage | Early-stage to scaling businesses | Mature, established businesses |

| Typical cheque pattern in UAE | Early to growth rounds, often with follow-on expectations | Larger transactions in established companies, often tied to control or significant influence |

| Ownership style | Minority stake, typically less than 50% | Majority or full control, often above 75% |

| Operating role | Advisory, board involvement, strategic support | Hands-on restructuring, operational influence, often debt-backed |

| Return logic | Outlier wins drive fund performance | More consistent value creation through control and operational improvement |

| Founder fit | Builders chasing speed, category leadership, regional scale | Operators who value structure, efficiency, ownership transition, or liquidity |

Cheque size matters less than the strings attached

Founders usually ask about cheque size first. Fair enough. Cash changes your options. But the more useful question is what that capital commits you to over the next three to five years.

In the UAE, venture rounds can range from smaller seed cheques to multi-million-dollar growth rounds, with firms in the region actively backing startups from seed through Series B, as tracked by MAGNiTT's MENA investor and funding data. The practical point is simpler than the headline number. VC money usually assumes there will be another round, a bigger story, and a much larger company on the other side.

PE capital usually enters once the business can withstand heavier diligence, tighter reporting, and sharper scrutiny on unit economics, management depth, and cash generation.

Practical rule: Do not ask only, “How much can I raise?” Ask, “What operating cadence, governance standard, and future financing path comes with this money?”

Expectations show up in your calendar

The return model changes your weekly life as a founder.

VC investors can tolerate mess for longer if growth is strong enough. They will sit through product resets, aggressive hiring, market entry bets, and short-term losses if they believe the upside is large. That sounds founder-friendly until the board starts measuring every quarter against a venture trajectory your company may or may not want.

PE investors usually have less patience for narrative and more interest in execution. Reporting packs matter. Management layers matter. Margin improvement matters. If performance slips, the discussion gets operational very quickly.

That is why the Founder Decision Matrix matters here. The choice is not only about stage. It is also about temperament. Founders who like experimentation, ambiguity, and repeated fundraising cycles usually cope better with VC. Founders who prefer process, control over pace, and a business that gets stronger through disciplined execution often find PE logic easier to live with.

If you want a grounded view of how buyers and investors in the region assess that shift, this Q&A from UAE private equity experts is worth reading.

Control is where the relationship really changes

Before the video, focus on the part many founders underestimate.

VC firms typically buy enough equity to matter, but not enough to run the company day to day. They influence through board seats, investor rights, follow-on decisions, and pressure around growth milestones. You still feel like the driver, even when the board is demanding.

PE is different. Control is often the point. A PE investor may want majority ownership, authority over major decisions, and the ability to change leadership, cost structure, or strategy if the numbers require it. That summary aligns with this overview of Differences in private equity and VC.

Some founders are comfortable with that. Others hate it, even when the valuation is attractive.

The personal side of the decision now becomes tangible. If your best work happens when you have room to improvise, PE can feel restrictive very fast. If you are tired of carrying everything yourself and want a partner who will institutionalise the company with you, PE can be a relief.

Exit pressure feels different in each model

VC pressure is usually about scale. A company that becomes profitable but tops out as a solid regional business may still disappoint a venture fund that needs a few outsized outcomes to return the fund.

PE pressure is usually about performance against plan. The questions are more direct. Did margins improve? Did cash conversion improve? Did the business become more valuable on a measurable basis?

For founders, both paths create pressure. The difference is the kind you can live with.

VC suits founders who want speed, can handle dilution across multiple rounds, and are willing to build with the expectation of a large exit. PE suits founders who want liquidity, operational support, or a transition from founder-led hustle to institutional execution. That is why the right choice in the UAE is rarely “which investor pays more?” It is “which capital model fits the business and the founder I am?”

Founder Stories from the UAE Ecosystem

A founder in Dubai raises a strong round, hires fast, opens Saudi conversations, and suddenly spends more time in board prep than with customers. Another founder takes capital later, keeps tighter control, adds systems, and grows at a pace that still lets him sleep. Both made rational choices. They just chose different lives.

That is the useful lens here.

In the Founder Connects WhatsApp group, the honest conversations are rarely about whether VC or PE sounds more prestigious. Founders talk about what changed after the term sheet. Who started reporting weekly. Who had room to test. Who had to accelerate expansion before the company was fully ready. Who felt relieved once an investor brought structure.

Aisha chose VC because speed mattered more than control

Aisha built a Dubai AI SaaS company selling into enterprise teams across the GCC. She had a real product, early customer pull, and a market that would not stay open forever. Her main problem was not operational discipline. It was time.

Dubai continues to attract a large share of regional startup capital, and platforms like MAGNiTT regularly track how concentrated MENA tech funding is in the UAE. For a company like Aisha's, that matters. There is an active pool of venture investors looking for software businesses that can expand across the region before the category settles.

So the VC case was straightforward. Raise early enough to hire ahead of revenue, build enterprise sales properly, and push into adjacent GCC markets before a slower competitor catches up.

What changed after the round was predictable:

- Hiring moved earlier. She brought in senior product and sales talent before the business would have funded those roles on its own.

- Decision-making became more scheduled. Monthly reporting, pipeline scrutiny, and hiring plans all tightened.

- The company stopped being judged as a good UAE business. It was judged on whether it could become a regional winner.

- Exit planning showed up much earlier in strategy discussions, even while the product was still evolving.

She got the upside she wanted. Speed, signal, and a stronger shot at market share. She also accepted the founder job that comes with VC. More dilution, more visibility, and less room to grow slowly.

Karim chose PE because he wanted a better business, not a venture story

Karim ran a healthy food café chain with solid unit economics, repeat customers, and a brand people knew. He was not pitching a category-defining tech narrative. He was building a real operating business with procurement issues, store rollout decisions, margin pressure, and a management bench that needed strengthening.

That profile often struggles in VC rooms. The questions keep coming back to venture-scale upside, even when the underlying company is healthy.

Karim wanted something else. He wanted to expand carefully, professionalise the business, and possibly take some liquidity without turning every decision into a bet on hypergrowth. That pushed him toward PE style capital.

The questions he asked were different from Aisha's:

- How much board and veto control will the investor ask for?

- Can I stay CEO, and for how long?

- Are they backing expansion, buying secondary shares, or both?

- Will they improve the finance function and reporting, or just demand it?

- What does a good outcome look like if we build a larger GCC business without becoming a unicorn?

Those are not small questions. They shape the founder's day-to-day life after the deal closes.

A founder with a profitable company and measured ambition should not force a venture narrative to fit startup fashion.

The real lesson is personal

Aisha and Karim did not just pick different sources of capital. They picked different operating identities.

Aisha chose a path that rewards ambition, speed, and comfort with repeated fundraising pressure. Karim chose a path that suits an operator who values control, durability, and tangible business improvement.

That is why the Founder Decision Matrix matters. The right answer is not only about revenue growth, margins, or valuation. It is also about temperament. Some founders do their best work with urgency, public milestones, and a big regional swing. Others build better businesses with tighter control, steadier execution, and a partner who cares more about operating quality than headline growth.

In the UAE, both paths can work. The mistake is choosing the capital style that flatters your ego instead of the one that fits how you want to build.

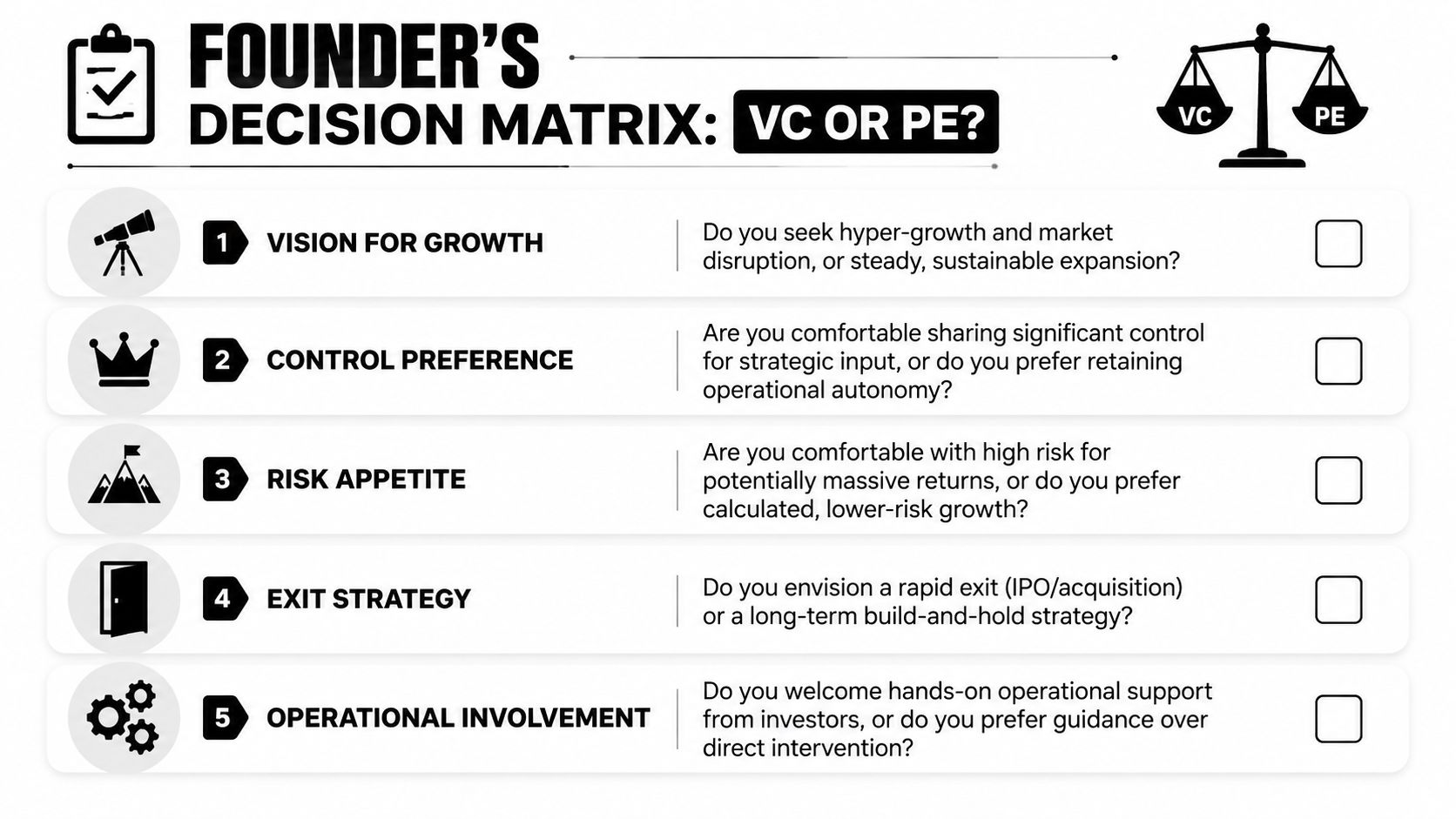

The Decision Matrix Are You a VC or PE Founder

Most founders try to answer this with revenue metrics alone. That's incomplete. The sharper test is personal.

Start with founder personality, not deck language

Use this matrix accurately.

| Question | If your answer is mostly this | You likely lean |

|---|---|---|

| What do you want to build? | A market leader that scales fast across MENA | VC |

| A strong, durable business with controlled expansion | PE | |

| How do you feel about dilution? | Comfortable giving up more ownership for speed | VC |

| Prefer tighter ownership economics and structured control conversations | PE | |

| What kind of investor help do you want? | Strategic intros, signal, hiring support, board guidance | VC |

| Operational discipline, governance, restructuring, expansion planning | PE | |

| What kind of pressure can you handle? | Fast targets, future rounds, big outcome expectations | VC |

| Deeper oversight, more control from investors, execution discipline | PE | |

| What life do you want as a founder? | Intense sprint with a clear exit path in mind | VC |

| Longer operating journey, possibly with partial liquidity or ownership transition | PE |

Five blunt questions to ask yourself

- Do you want hyper-growth, or do you want a very good business? These are not the same thing.

- Would you trade control for speed? Many founders say yes in a pitch meeting and no once governance gets real.

- Do you like uncertainty? VC lives with more of it. PE tries to reduce it.

- Are you trying to dominate a category or professionalise an operation? Your answer changes who should be on your cap table.

- Do you want an exit, or do you want optionality? Investors care because their incentives sit on a timeline.

The UAE crossover point matters

There's a specific nuance in this region that founders miss. Global benchmarks often suggest PE becomes relevant around $5M to $10M in revenue, but in the UAE and MENA that crossover often shifts to $15M+ revenue because of fragmented markets and local compliance requirements, as explained in this analysis of private equity vs venture capital UAE trends.

That gap creates a real founder problem. You may be too mature for classic VC enthusiasm, but still too small or too regionally messy for PE.

When that happens, don't force the label. Instead:

- Clean your reporting: monthly reporting quality often matters before investor appetite changes.

- Clarify your use of funds: expansion, buyout, working capital, or partial liquidity are not the same ask.

- Build investor-fit materials: a VC deck and a PE memo should not sound identical.

- Prepare for a waiting period: some businesses need more time to become financeable by the right class of investor.

Founder test: If your dream outcome is “build carefully, stay profitable, and own a meaningful chunk for a long time”, you probably don't want venture pressure no matter how attractive the headline valuation looks.

Your Next Step Choosing The Right Capital Partner

Once you know which path fits, the next move is execution. Don't turn this into another abstract strategy exercise.

Do these three things this week

Write a one-page funding brief

Not a deck. A one-pager. State the amount you want, what it funds, what ownership outcome you can live with, and what investor type fits.List your essential requirements on control Often, deals falter at this stage. In the UAE, VC firms typically take minority stakes below 50% and act as advisers, while PE firms usually seek majority control above 75% to restructure operations and utilize debt financing, based on this regional explanation of PE and VC control differences. If you haven't decided where you stand on control, you're not ready for either conversation.

Pressure-test your materials with founders, not just advisers

Ask someone who has already taken the kind of money you're considering. They'll tell you what the investor promised, what changed after closing, and what they wish they'd negotiated harder.

Prepare for diligence before it starts

Good founders don't wait for a term sheet to get organised. They clean contracts, cap table records, board approvals, key policies, and commercial documentation early. If you need a practical primer on what investors and buyers will inspect, this guide on navigating business due diligence is worth reviewing before meetings get serious.

If you're going down the venture route, sharpen your negotiation prep as well. These VC negotiation tactics for getting better terms as founders are a useful starting point.

Keep the capital search narrow and relevant

Don't spray your deck across the market. Build a short list by business model, stage, geography, and investor behaviour. For UAE tech founders, tools like investor databases, warm founder intros, and targeted communities can help. Founder Connects is one example. It gives founders a way to meet peers, compare notes off the record, and get more relevant introductions before they waste time in generic fundraising loops.

The right capital partner should make your company more itself, not force it into someone else's template.

If you're weighing VC against PE and want candid founder-to-founder input, join Founder Connects. It's a private UAE and MENA founder community built for practical conversations, curated introductions, and the kind of honest feedback that helps you choose the right capital path before you sign the wrong deal.

Building in MENA? You don't have to do it alone.

Join 300+ founders in the Founder Connects Residency. Monthly squad calls, warm intros, $3M+ in perks, and much more. All for less than your monthly coffee budget.

Popular posts

The premier community for tech founders, investors, and builders. Connect, collaborate, and grow together.