Top IoT Startups Driving UAE Smart Cities

Building in MENA? You don't have to do it alone.

Join 300+ founders in the Founder Connects Residency. Monthly squad calls, warm intros, $3M+ in perks, and much more. All for less than your monthly coffee budget.

IoT is no longer a side tool in the UAE. It now sits inside city systems that deal with flooding, traffic, buildings, parking, logistics, and construction safety. After Dubai’s April 2024 storm led to about US$3 billion (around AED 11 billion) in insured losses, the case for connected sensors and live data became much harder to ignore.

If I had to sum up the article in one line, it would be this: the startups getting attention in the UAE are the ones solving one clear city problem, proving they can work on local sites, and showing a path to repeat revenue.

Here’s the article in simple terms:

- I see 10 names tied to the UAE smart-city push: e& UAE, Bayanat, Smart IoT LLC, DOTS, iBigData, Arnab, YallaParking, Derq, Fero.AI, and WakeCap

- The strongest themes are mobility, smart buildings, city sensing, geospatial data, logistics, and worker safety

- A lot of these firms grow by adding sensors and software to sites that already exist, instead of rebuilding from scratch

- In the UAE, growth often depends on pilots, public-sector access, telecom links, and PaaS or subscription income

- Some firms already show hard market signals, such as US$6 million for Derq and US$28 million Series A for WakeCap

- The article also points to market support from LoRaWAN access, state-backed programmes, and UAE startup funding activity

What stands out most to me is how mixed this group is. Some sit at the network layer. Some work in city data. Others focus on buildings, roads, parking, or worksites. So this is not one narrow IoT story. It is a city-systems story.

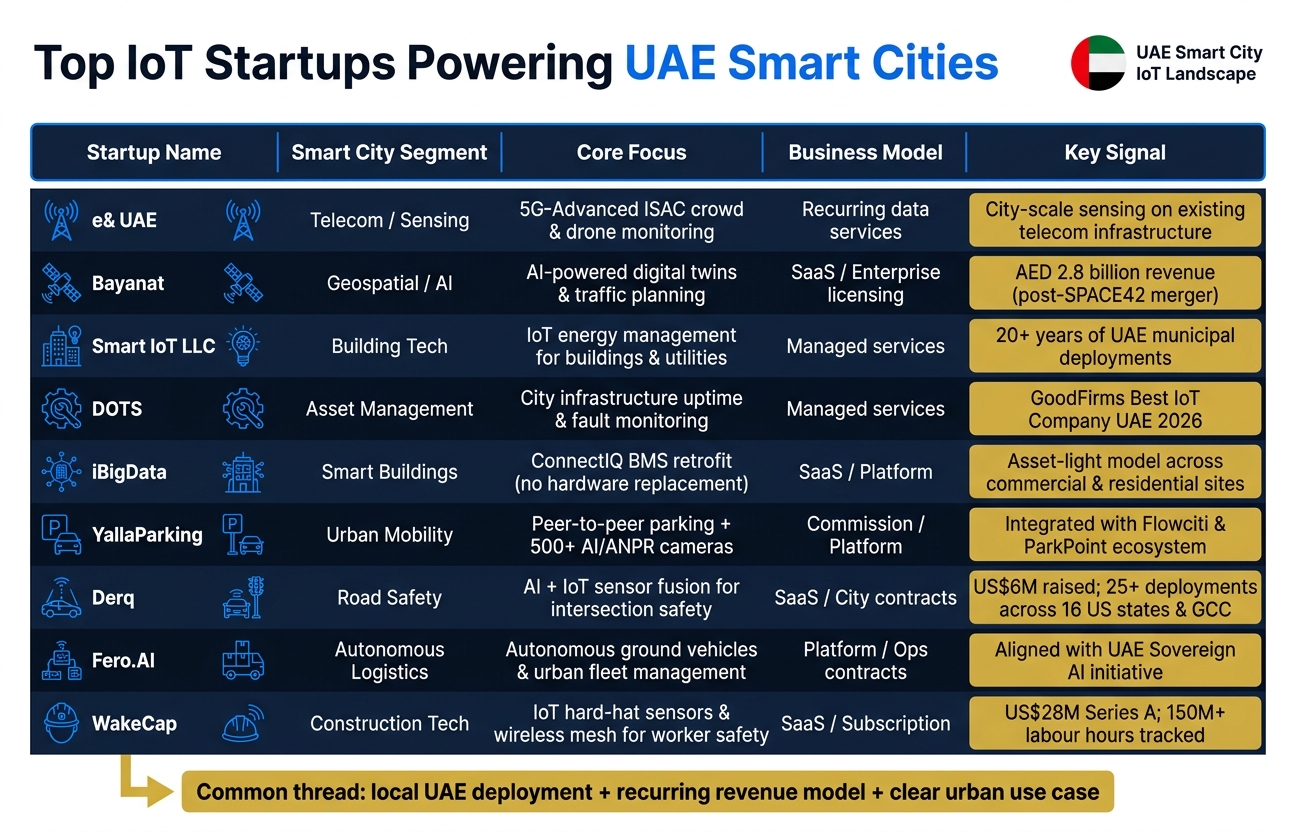

Top IoT Startups Powering UAE Smart Cities: At a Glance

Inside Expo City Dubai: How AI Runs a Smart City in Real Time - PTF

Quick Comparison

| Startup | Main focus | UAE smart-city role | Clear signal |

|---|---|---|---|

| e& UAE | 5G sensing | Crowd, occupancy, drone monitoring | Uses existing telecom network for sensing |

| Bayanat | Geospatial AI | Traffic, assets, planning | Part of SPACE42; AED 2.8 billion revenue noted |

| Smart IoT LLC | Energy management | Building and utility control | 20+ years in Dubai |

| DOTS | Asset monitoring | City infrastructure uptime | UAE market presence and sector award |

| iBigData | Building systems integration | Retrofit building control | Works without full hardware replacement |

| Arnab | Not clear from source | Not confirmed | No verified UAE deployment or funding shown |

| YallaParking | Parking marketplace | Parking access and mobility data | 500+ AI cameras and ANPR use |

| Derq | Road safety | Intersection risk detection | US$6 million funding; GCC and US deployments |

| Fero.AI | Autonomous logistics | Fleet and urban logistics tasks | Tied to UAE interest in sovereign AI systems |

| WakeCap | Construction IoT | Worker safety and site tracking | US$28 million Series A; 150 million+ labour hours tracked |

Bottom line: if you want to understand where UAE smart-city IoT is heading, I’d look at the firms that can prove local deployment, cut rollout friction, and keep billing after the first install.

Why IoT Startups Matter in the UAE Smart City Push

Demand from Smart Dubai, Abu Dhabi and Masdar City

Programmes in Smart Dubai, Abu Dhabi and Masdar City create direct procurement demand for connected infrastructure across mobility, energy, water, and building management.

You can see that demand in live projects. FortyGuard's Masdar City deployment points to a need for heat analytics that help guide cooling, materials, and operations.[3] These programmes also depend on local operational data to support day-to-day decisions. That creates room for startups that can move fast, deploy in the field, and show city-level impact without a long lead time.

Why Startups Move Faster Than Large Vendors

The main edge is the overlay model. Instead of rebuilding city assets from scratch, startups add connected sensors and software on top of what is already there.

That approach cuts time, cost, and disruption. SRMES, for example, built an IoT rainwater system that triggers drainage gates and sends real-time alerts. A pilot for one neighbourhood was estimated at AED 300,000.[1] Syncrow took a similar route with its SyncOS platform, launched in July 2025, which integrates more than 60 device types to update building management in Dubai and Riyadh without structural changes. The platform also supports UAE Green Agenda 2030 targets.[2]

That said, pilots do not scale on product alone. They still need network access and enterprise partners to move beyond a small rollout.

How Funding and Partnerships Shape Growth

Public infrastructure is making deployment easier for UAE tech startups. Digital DEWA's ICT arm, InfraX, offers nationwide LoRaWAN connectivity, so startups can deploy sensors without building their own communications layer first.

Dicode Technologies used that exact model in October 2024, partnering with InfraX to roll out smart gas metering at scale through a Platform-as-a-Service (PaaS) structure. The result: deployment costs for utilities fell by up to 30%.[6]

The funding climate also helps. The UAE led MENA startup funding in May 2026, securing $379 million.[3] Then in June 2026, telecom operator du launched a $50 million venture capital fund to back startups tied to digital growth.[3]

Put those pieces together and the pattern is clear: network access, public-sector support, and capital make it easier for startups to move from pilot stage to broader rollout. The startups below match that pattern with a clear use case, local deployment, and a path to scale.

What Makes an IoT Startup Stand Out in UAE Smart Cities

Not every connected device company should make this list. The startups here were picked using three simple filters. In a market shaped by procurement cycles and access to capital, proof in the field matters more than polished product claims. The goal was to focus on startups with real traction in the UAE, not just smart-device ideas on paper.

A Clear Urban Use Case

The strongest IoT startups tend to solve one clear city problem instead of trying to do everything at once. That focus matters. City buyers usually want tools that fix a specific issue and plug into systems they already use.

Tuqa Alabdouli, Founder and CEO of SRMES, said it in plain terms:

"We should have a proactive system not a reactive one so people are safer." [1]

That kind of focus tends to land better with public-sector buyers than broad, catch-all pitches.

Visible UAE Market Presence

Local pilots carry weight because UAE conditions can expose hardware flaws and maintenance gaps very fast. Heat, dust, heavy usage, and site demands can punish weak products. So this list gave priority to companies with live UAE deployments, active pilots, or confirmed partnerships.

Syncrow is one example. It launched its SyncOS platform in July 2025 and supports more than 60 device types across hospitality, healthcare and government sectors. [2] That kind of footprint in the UAE points to real market commitment, not just intent.

Deployment and Investment Signals

Market presence alone isn't enough. The list also looks for signs that a startup can grow without hitting a wall. That includes partnerships, programme wins, and pricing models that reduce upfront adoption costs. A move away from one-time hardware sales and towards subscription or PaaS models can make rollout easier.

Programme selection is another strong signal. SRMES, for example, was chosen as one of 10 winners from 148 applications and awarded an AED 50,000 grant by the Expo City Dubai Foundation's Changemakers Academy. [1]

That’s usually the kind of profile city buyers and investors look at first.

The startups below meet these checks through live UAE deployments and clear urban use cases.

1. Etisalat Digital

Etisalat Digital, now part of e& UAE, shows where UAE smart-city IoT is heading. The shift is no longer just about connected devices. It’s moving up to the network itself.

The company is turning its 5G-Advanced network into a sensing layer through Integrated Sensing and Communication (ISAC). In simple terms, that means the network can detect activity without relying on cameras or extra spectrum. It uses existing infrastructure and keeps the sensing model privacy-conscious. In October 2025, e& UAE and Tiami Networks showed this in action at GITEX Global in Dubai. Using the PolyEdge platform, they tested crowd analytics, occupancy detection, and drone monitoring over existing 5G-Advanced infrastructure.[9]

e& UAE says this model is a step towards safer, smarter operations across airports, venues, and energy sites.[9]

What stands out here is the recurring-revenue angle. e& UAE is building towards recurring sensing data services, with ongoing income tied to real-time operational data for enterprises and government users across airports, venues, and city operations.[9]

That matters because the upside for UAE smart cities isn’t just new hardware. It’s scalable, real-time operational data without rolling out new camera networks or tearing up sites for major rebuilds. For investors in the UAE, the message is pretty direct: city sensing can sit on top of existing telecom infrastructure and still support operations at scale.[9]

This infrastructure-led model also shows a clear path for UAE IoT growth. Start with the network layer, then extend into city applications.

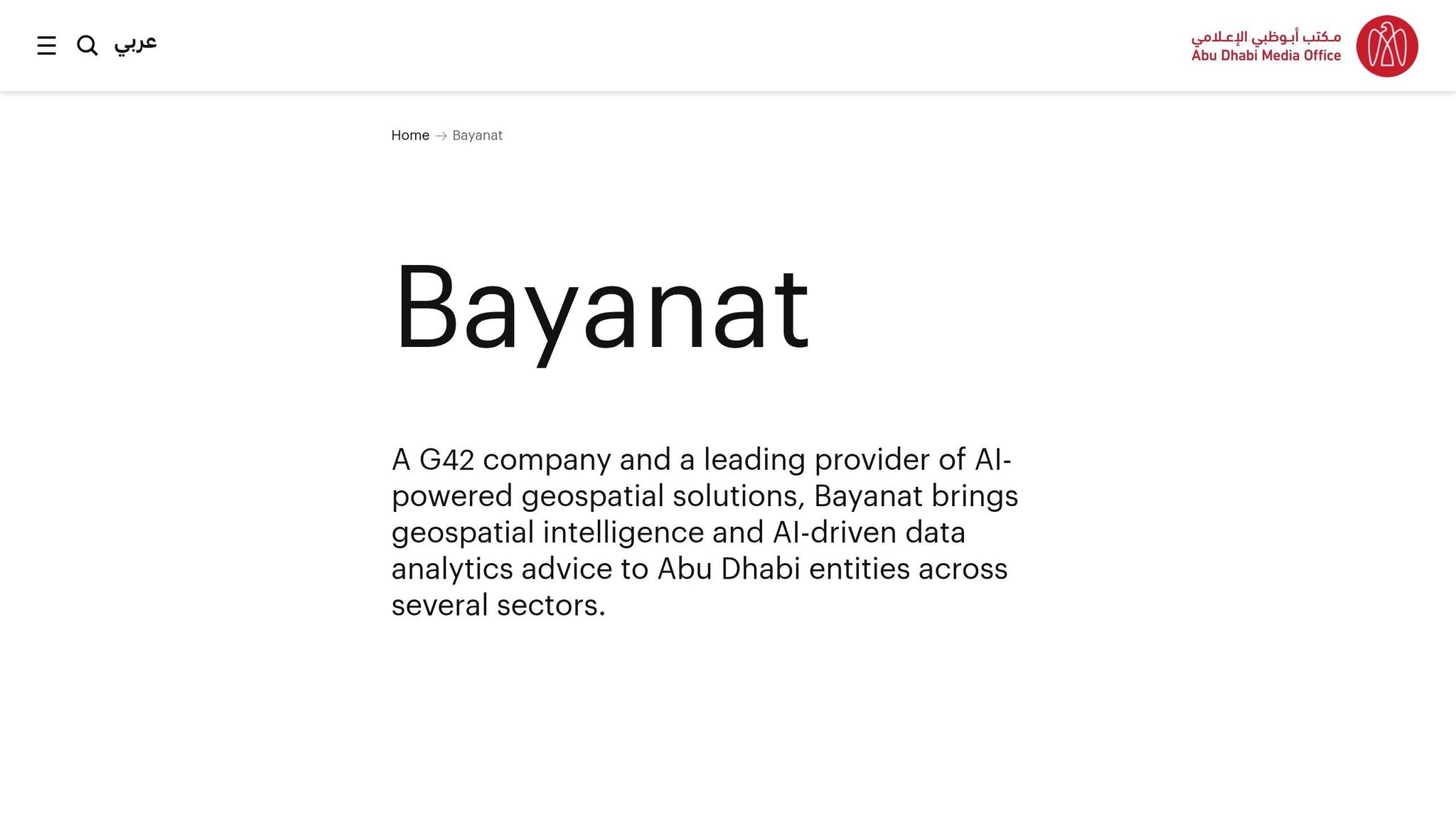

2. Bayanat

Bayanat turns geospatial and satellite data into practical city decisions. The company focuses on AI-powered geospatial solutions, including digital twins, Earth observation, and mobility solutions.[10] Its main platform, GIQ, brings together space and ground data to support day-to-day decision-making for government and enterprise clients.[12]

That matters because city teams don’t just need data. They need data they can use. In Bayanat’s case, that means support for traffic planning, asset management, and infrastructure planning. So the company fits into the parts of city work that depend on better planning, faster response, and smoother operations.

Bayanat’s merger with Yahsat created SPACE42, a space-and-AI company. The combined entity reported revenue of AED 2.8 billion and net income of AED 639 million in 2023.[10]

One part of Bayanat’s offering stands out for government use: DigiGov. This framework helps public-sector entities use geospatial analytics on top of cloud infrastructure to improve operations, policy, and resource use.[11] In May 2024, Bayanat signed an MoU with Tata Consultancy Services to bring digital twin and geospatial analytics into sustainability tools.[11]

In the smart-city stack, Bayanat sits closer to the city data layer than the device layer. That places it alongside the hardware-led startups coming next, while also marking a clear shift in this article - from network-led sensing to data-led city intelligence.

3. Smart Iot LLC

Smart Iot LLC sits at the day-to-day operating layer of UAE smart cities, linking city-scale data with building-level control. Founded in 2003 and based in Dubai, the company builds IoT energy management systems for commercial and residential properties. In plain terms, that puts it close to the parts of a city that affect building efficiency, utility control, and grid integration across the UAE.

It also works with Carl Data Solutions, now infinitii ai, on environmental monitoring services in the UAE. The setup combines sensors with analytics for industrial and municipal clients. That matters for municipalities that need systems that can work in the field, not just data shown on a screen.

Smart Iot LLC is privately held and unfunded, with a team of 6 to 49 people. More than 20 years in Dubai gives it the profile of a steady municipal partner. Its unfunded status also suggests a bootstrapped operator, rather than a venture-scaled platform.

4. DOTS

While Smart Iot LLC works at the building level, DOTS looks across the city. DOTS Tech Systems LLC is a Dubai-based IoT provider focused on city assets, infrastructure monitoring, and machine visibility. In simple terms, it sits in the asset-management layer of UAE smart cities, where uptime and fast response times matter.

DOTS has a 50–249 employee base and an established UAE footprint. GoodFirms recognised it in 2026 as a Best Internet of Things Company in the UAE[13]. That kind of operating base makes DOTS a stronger fit for public-sector rollouts than for small pilot projects.

The market case is clear, and DOTS’s focus on asset monitoring lines up well with Dubai’s IoT Strategy and data platforms such as Dubai Pulse[13][14]. For investors, the path to scale is straightforward: public-sector growth calls for a mainland presence and TDRA approval.

5. iBigData

If the last startup was about city assets, iBigData goes a level deeper: the buildings those systems rely on. Based in Dubai and operating as IOT Big Data IT services LLC, the company focuses on smart building use cases [13].

Its ConnectIQ platform brings fragmented building management systems into a single control layer. It works with major BMS systems, including Honeywell, and does that without a full hardware replacement [13]. That matters for owners who want to upgrade older sites without ripping out the core setup.

The result is simple. The retrofit model lowers upgrade costs and helps buildings use energy better.

iBigData also keeps a lean setup, with 2 to 9 employees, while aiming for repeatable rollouts across commercial and residential sites [13]. A small team can be an advantage here. It keeps delivery tight and makes it easier to repeat the same installation model across multiple properties.

For investors, the appeal is clear: a retrofit-led model that reduces adoption costs and lines up well with UAE real estate demand [13].

sbb-itb-f597d8f

6. Arnab

Current sources don’t show verified UAE deployment or funding data for Arnab.

The next startups have clearer signals around deployment, product, and funding.

7. YallaParking

YallaParking turns idle private parking into part of the mobility network in busy UAE areas. It connects drivers with property owners who have spare spaces through a peer-to-peer marketplace. In packed districts like JBR and Downtown Dubai, that matters a lot. Parking stops being just a space on the ground and starts working like a live data layer for city operations.

The platform also ties into a bigger mobility setup. Through its integration into the Flowciti Group and ParkPoint ecosystem, YallaParking connects parking management with broader urban mobility systems.[4] That means parking isn't treated as a silo. It becomes part of the infrastructure that helps people move through the city.

On the operations side, YallaParking uses more than 500 AI-powered curbside and pole-mounted cameras with ANPR to read number plates, track duration, and flag violations without manual intervention.[15] In plain terms, the system can monitor parking activity at scale without relying on on-site staff to check every vehicle.

Its business model is asset-light because YallaParking does not own real estate. Instead, it takes a commission on each booking. Private parking spaces in prime Dubai locations typically rent for around AED 250 to AED 500 per month.[16] The platform also handles electronic access passes and security deposits, linking digital bookings with building access.[16] That combination of recurring commission income, low capex, data, and automation gives the company room to scale without having to buy parking assets itself.

8. Derq

Derq focuses on one clear smart-city challenge: stopping road accidents at intersections. The company, an MIT spin-off, uses AI, computer vision and IoT sensor fusion to predict traffic accidents in real time by analysing live intersection video. It also supports connected infrastructure, traffic control and vehicle-to-everything (V2X) use cases. [17][19][20]

In Dubai Silicon Oasis, Derq and DIEZ installed 14 AI Smart Pedestrian Crossing Systems in August 2023 after two years of testing. The project runs on du's 5G MEC setup, which helps with low-latency remote operation and data collection. [20][21] That on-the-ground validation later helped back its funding round.

In October 2024, Derq raised $6 million, led by e& capital and AT&T Ventures. The company holds 17 patents and has more than 25 active deployments across 16 US states and the GCC. [17][18][19]

For city buyers and investors, that mix matters. It shows Derq isn't just selling an idea on paper; it's already working in live urban settings. For UAE smart city projects, the company sits in the mobility and safety layer, covering pedestrian protection, cyclist safety, congestion control and real-time risk prevention. In practical terms, that places Derq in the real-time urban operations layer of UAE smart cities. [17][22]

9. Fero.AI

Road safety and parking get a lot of attention. But in the UAE, smart city plans also reach into autonomous logistics. Fero.AI builds autonomous ground vehicles and smart logistics systems that use connected data to automate urban operations. That puts the company in the city operations layer, where automation can cut cost and reduce exposure in day-to-day logistics.

The UAE's Sovereign AI push is also adding weight to demand for locally controlled systems in ports, logistics, and transport. That makes this category more relevant for public-sector buyers. [8]

For city buyers, the appeal is practical, not abstract. They want live pilots, clear efficiency gains, and systems that are ready to deploy. That’s where Fero.AI starts to stand out in day-to-day use, especially for fleet management, logistics efficiency, and safer infrastructure operations. [23]

10. WakeCap

Smart cities don’t begin when the skyline is done. They begin on the construction site.

WakeCap brings that idea into practice by turning job sites into live data environments. Founded in 2017 and based in Dubai Production City, the company places IoT sensors inside hard hats without forcing teams to change how they already work. Its patented wireless mesh network runs without GPS, Wi‑Fi, or heavy cabling [24][25][26][27]. That means construction IoT becomes part of the smart city build process itself, not some side category.

You can see that in how the platform is used on active sites. WakeCap connects with tools such as Oracle and OpenSpace, feeding a centralised dashboard that shows worker presence, safety events, and site productivity in one place [24][28]. So instead of piecing updates together from different systems, project teams get a live view of what’s happening on the ground.

The scale is hard to ignore. WakeCap has tracked more than 150 million labour hours across major projects around the world [27][29][30]. Its client base includes Emaar and major regional giga-projects, and major Saudi entities require its safety solutions across their sites [27][30]. Reported results include a 91% drop in safety issues and 70% faster incident response times [28][29].

That momentum has drawn investor interest too. In June 2026, WakeCap acquired Frontline Industrial Software to connect AI planning with live site data [24]. Earlier, in May 2025, the company closed a US$28 million Series A, led by UP.Partners, bringing total funding to US$31.55 million. Its backers include Aramco Ventures and Wa'ed Ventures [24][28].

Funding Outlook for UAE Smart City and IoT Ventures

The startups featured here sit across five smart-city layers, and they don’t all fund the same way. That tracks with the market itself: device-led companies tend to scale one way, while analytics-led firms often follow another path.

Which IoT Segments Attract Capital

AI-led city analytics is pulling in the biggest rounds. Core42’s US$550 million raise to expand AI infrastructure in the UAE shows where large investors are putting money [4]. In the same space, Abu Dhabi-based Origen secured US$50 million from BlueFive Capital in July 2026 to scale production AI for government and smart-home use cases [31].

Smart buildings and PropTech are also getting solid attention, especially around decarbonisation and resource efficiency. A good example is the DIFC Innovation Hub’s Global Landing Pad Programme, which brought in six scale-ups in July 2026 - including Watergate AI and UTwin - to work with regional developers such as Majid Al Futtaim and Sobha Realty [5].

Urban mobility still draws investor interest too, mainly in platforms that bring together parking management, EV charging infrastructure, and super-app logistics in one place [7].

Common Funding Routes in the UAE

| Funding Route | Typical Stage | Example | Range |

|---|---|---|---|

| Grants | Ideation / MVP | Expo City Dubai Foundation's Changemakers Academy | AED 50,000 [1] |

| Seed VC | Early growth | PRYPCO | around US$10 million [32] |

| Venture round | Scaling | 1001 AI | US$30 million [5] |

| Debt financing | Mature / industrial | Qashio | US$32.3 million [32] |

Money tends to follow proof, not pitch decks. For hardware-heavy IoT startups, that often means moving through procurement cycles, pilot programmes, and utility partnerships before venture firms step in.

What Investors Look For Before Backing IoT Startups

Investors usually want to see field performance first. It’s not enough for a sensor to work in a lab; it has to hold up in heat, dust, and day-to-day city conditions. Once hardware reliability is clear, attention shifts to recurring revenue - often through PaaS or subscription models - and fit with D33 and UAE Net Zero 2050.

In practice, that means buyer access, pilot deals, and founder networks can matter just as much as the product.

Where Founders Can Plug Into the UAE Startup Community

Why Community Access Matters for IoT Founders

After pilots and funding signals, founder access often becomes the next bottleneck. Getting something to work in a lab is one thing. Getting it deployed in the UAE, clearing approvals, and landing municipal pilots is a different game.

That’s where the right founder network helps. Peer access can shorten the path from prototype to municipal pilot. And in IoT, that matters a lot, because UAE field conditions tend to expose hardware gaps fast.

Founder Connects for Networking and Investor Access

For founders who want faster feedback and warmer introductions, Founder Connects is one useful way in. The platform brings together more than 250 UAE-based founders and has supported 98 documented collaborations. Its members have also raised a combined AED 189 million in funding [33].

What does that look like in practice? Founder Squads, weekly introductions, live talks, expert advice, and a curated investor list all help founders move with less friction.

For founders building in smart city and IoT, two tools stand out:

- The UAE Investor Match Finder is free to use and does not require sign-up.

- The UAE Startup Ecosystem Analyser helps founders line up their solutions with current market demand [33].

For IoT founders, Founder Connects offers a direct path to peers, pilot opportunities, and investor access.

Comparison Snapshot of the Featured Startups

Segment and Scaling Comparison

The table below shows where these startups sit, what they do, and how they grow.

| Startup | Segment | Core Solution | Primary Smart City Use Case | Business Model | Scaling Signal |

|---|---|---|---|---|---|

| e& UAE (Etisalat Digital) | Telecom / Sensing | 5G-Advanced ISAC sensing layer | Crowd analytics, occupancy detection, drone monitoring | Recurring data services | City-scale sensing on existing telecom infrastructure [9] |

| Bayanat | Geospatial / AI | AI-powered geospatial and digital twin platform | Traffic planning, asset and infrastructure management | SaaS / enterprise licensing | AED 2.8 billion revenue post-SPACE42 merger [10] |

| Smart IoT LLC | Building Tech | IoT energy management systems | Building efficiency and utility control | Project-based / managed services | 20+ years of UAE municipal deployments |

| DOTS | Asset Management | City asset and infrastructure monitoring | Uptime management and fault response | Managed services | GoodFirms Best IoT Company UAE 2026 [13] |

| iBigData | Smart Buildings | ConnectIQ BMS integration platform | Retrofit building management without hardware replacement | SaaS / platform | Asset-light retrofit model across commercial and residential sites [13] |

| YallaParking | Urban Mobility | Peer-to-peer parking marketplace with ANPR cameras | Parking management and urban mobility data | Commission / platform | 500+ AI cameras; integration with Flowciti and ParkPoint [15] |

| Derq | Road Safety | AI and IoT sensor fusion for intersection safety | Pedestrian protection and real-time risk prevention | SaaS / city contracts | US$6 million raised; 25+ deployments across 16 US states and GCC [17][18] |

| Fero.AI | Autonomous Logistics | Autonomous ground vehicles and smart logistics systems | Urban logistics automation and fleet management | Platform / operations contracts | Aligned with UAE Sovereign AI push [8] |

| WakeCap | Construction Tech | IoT hard hat sensors and wireless mesh network | Worker safety and site productivity tracking | SaaS / subscription | US$28 million Series A; 150 million+ labour hours tracked [24][28] |

A clear pattern stands out. Infrastructure, utilities, and building-tech firms often scale faster because they deal with repeat operational pain points. That matters. If a startup helps a city cut energy waste, manage assets, or keep buildings running better day after day, demand tends to stick.

The business model tells part of the story too. SaaS, PaaS, and data monetisation models usually point to steadier repeat revenue than one-time hardware sales. In plain terms, investors often like businesses that keep billing after the first deployment instead of starting from zero with each new deal.

That’s why these differences matter so much. Segment, use case, and go-to-market model all shape how investors look at risk, revenue headroom, and how fast a startup can move from pilot stage to city-wide rollout.

Conclusion

Taken together, this list shows where UAE IoT startups are heading: away from one-off pilots and into city infrastructure.

And the opportunity is broad. It spans drainage, parking, road safety, smart buildings, construction, and urban sensing. That's a big range, but the thread running through all of it is simple: these companies are working on city problems that need to be solved on the ground, not just talked about.

One pattern stands out across the startups featured here. They share a clear fit with day-to-day city needs. Each one focuses on a specific problem, uses deployable tech, and has a path to scale.

Recent funding momentum also points to strong investor appetite for UAE smart-city IoT.

What happens next comes down to a few plain factors: faster pilots, patient capital, and products built for city-wide deployment. That's how IoT startups move from testing phase to the systems cities rely on every day.

FAQs

Why is retrofit IoT important in the UAE?

Retrofit IoT matters in the UAE because it helps turn existing buildings into smarter, more sustainable, and compliant spaces without the cost and disruption of replacing whole systems.

That’s a big deal in a market where many properties need to meet stricter rules while still keeping day-to-day operations running smoothly.

It also gives property managers access to automated monitoring and predictive maintenance. In plain terms, they can spot issues earlier, fix problems before they grow, and stay on top of compliance needs with less guesswork.

The upside is clear: fewer risks, less chance of major penalties, and better energy efficiency. At the same time, these upgrades support the UAE’s Net Zero goals by helping buildings use energy in a smarter way.

Which UAE IoT startup segments look most investable?

In the UAE, the most investable IoT startup segments sit around smart infrastructure and lower-resource operations.

High-potential areas include smart building management, waste management, and utility upgrades such as smart gas metering and rainwater management. Investors tend to back scalable, data-led platforms that turn cost centres into revenue-generating assets while lining up with the UAE’s green and digital goals.

What helps an IoT pilot scale into a city-wide rollout?

Scaling an IoT pilot across a city usually comes down to cross-sector partnerships. Startups need to work closely with government bodies and private stakeholders to move through approvals and connect data across fragmented systems. Without that coordination, even a strong pilot can stall.

They also need solid sensing protocols, clear data requirements, proven impact in stable urban testbeds, and a business model that can scale without falling apart as deployment grows.

Founder Connects can help on that front through networking, expert resources, and access to funding.

Related Blog Posts

Building in MENA? You don't have to do it alone.

Join 300+ founders in the Founder Connects Residency. Monthly squad calls, warm intros, $3M+ in perks, and much more. All for less than your monthly coffee budget.

Popular posts

The premier community for tech founders, investors, and builders. Connect, collaborate, and grow together.