Startup Fundraising Process: A MENA Founder's Roadmap

Building in MENA? You don't have to do it alone.

Join 300+ founders in the Founder Connects Residency. Monthly squad calls, warm intros, $3M+ in perks, and much more. All for less than your monthly coffee budget.

Your runway is tightening. A few investors have said, “Keep me posted.” One mentor thinks you should start raising now. Another says wait until you've got stronger traction. Many first-time founders in the UAE lose months at this juncture. They either start too early with a weak story, or too late with too little cash left to control the process.

The startup fundraising process looks clean in generic blog posts. Build a deck, email investors, take meetings, sign a term sheet, close the round. In practice, especially in MENA, it's messier and far more relationship-driven. Investors are choosing carefully. Founders who win aren't always the loudest. They're usually the ones who show readiness, relevance, and trust long before the formal raise begins.

That's the roadmap worth following. Treat fundraising as a company-building process, not a pitch sprint.

Is Now the Right Time to Fundraise in MENA

The first question isn't “Who should I pitch?” It's “Am I ready to raise in this market?”

That matters more now because MENA startup funding weakened materially in 2024, with both deal volume and capital deployed declining versus prior periods, which means founders in the UAE are often raising in a more selective environment than generic startup advice assumes, according to this fundraising guide covering current market conditions.

Check readiness before you check your contact list

A lot of founders confuse urgency with readiness. Running low on cash is urgent. That does not automatically make the business investable.

Ask three blunt questions:

- Can you explain the next milestone clearly. Not “grow the business”, but something specific like shipping a critical product release, converting pilots into repeatable revenue, or proving retention in a defined customer segment.

- Can you show evidence, not ambition. Investors will listen to a vision, but they decide based on signals that you can execute.

- Do you still have enough time to run a real process. If your runway is too short, every conversation becomes desperate, and investors can feel that.

Practical rule: If you can't answer “what this round unlocks” in one sentence, you're probably not ready to start outreach.

When waiting is smarter than raising

Sometimes the right move is not to raise this month.

If your metrics are inconsistent, your co-founder situation is unresolved, or your story still depends on future promises, more meetings won't fix it. You're better off spending a focused stretch tightening product, cleaning up reporting, and lining up proof points that make the next conversation easier.

Founders should also sanity-check the broader capital picture. If you want a clearer view of how investor appetite and fund deployment shape timing, this note on VC dry powder and available capital in 2025 is useful context.

Signs it is time to go

There's no perfect moment, but there is a practical one.

You're closer when:

- Your narrative matches your stage. Early-stage investors don't expect perfection. They do expect coherence.

- Your customer evidence is improving. Even if the numbers are still small, the pattern should be credible.

- Your internal materials are nearly investor-ready. If someone asks for the deck, model, or core legal documents tomorrow, you shouldn't need weeks.

In MENA, timing is rarely just about the spreadsheet. It's about whether you can enter the market with enough proof and enough trust to give investors conviction.

Building Your Fundraising Groundwork Before You Pitch

A lot of founders in the UAE start pitching too early. They have a decent story, a half-finished deck, scattered numbers, and no clear answer for what this round will achieve. In this market, that usually ends the process before it properly starts.

Preparation does more than make you look organised. It helps investors build conviction faster. In MENA, where rounds often move through trusted introductions, peer checks, and repeated conversations, weak groundwork does real damage. One fuzzy meeting can travel through the network faster than one good deck.

In the region, pre-seed and seed rounds tend to follow a fairly clear progression, as outlined in Antler's overview of startup funding stages. The practical takeaway is simple. Raise for the next milestone, not for a five-year vision. If you are still proving retention, do not build a round story around regional expansion. If you are still testing pricing, do not present a model that assumes perfect sales efficiency.

Get the numbers that actually matter

Your materials should explain momentum in a way an investor can repeat to a partner after the meeting.

That standard is higher than it sounds.

For a product-led company, the useful metrics are usually around activation, retention, and whether usage keeps compounding after the first few weeks. For a B2B startup, investors usually care more about pilot-to-paid conversion, sales cycle length, expansion potential, and whether revenue is overly dependent on one or two accounts. For a marketplace, liquidity, repeat behaviour, and supply quality matter more than top-line traffic.

A lot of first-time founders make the same mistake. They export dashboards and call that preparation. Investors are not asking for raw reporting. They are trying to understand three things quickly:

- Is there real demand

- Can this team execute

- Is there a believable path to scale

If a metric does not help answer one of those questions, move it to the data room.

One more point matters in the UAE. Investors will often test your numbers informally through operator networks and founder references. If your reported momentum sounds polished but your customer behaviour is still weak, the gap shows up quickly. That is why disciplined reporting matters as much as headline growth.

Build a deck that carries the conversation

A strong deck does not try to say everything. It gives enough proof to earn the next meeting.

Guidance from Y Combinator's startup library on fundraising and pitch decks supports keeping the story concise and stage-appropriate. In practice, the best decks I see in MENA are short, clear, and easy for a partner to forward internally without extra explanation.

A practical deck usually needs these elements:

| Slide area | What investors need to understand |

|---|---|

| Problem | Why this pain matters now |

| Solution | What you built and why it fits the problem |

| Market | Where you can win first |

| Traction | Evidence that users or customers care |

| Business model | How value turns into revenue |

| Go-to-market | How you acquire customers in a repeatable way |

| Team | Why this team can execute in this market |

| Use of funds | What the round will be used for |

| Milestones | What should be true before the next raise |

Keep the sequence tight. Each slide should reduce doubt.

In MENA, the best decks also answer a question that is often left unsaid. Why will this company win here, specifically? That could be regulatory knowledge, local distribution, founder relationships, Arabic-language product depth, government access, or insight into how buying decisions happen in the Gulf. Generic startup logic is rarely enough on its own.

If you are still shaping the ask, it can help to review how different rounds are typically structured and timed. You can explore funding stages and financial steps before you finalise the amount, milestone plan, and dilution range.

Investors forgive an early product. They rarely forgive confused thinking.

It also helps to study how experienced founders position themselves to an investor in the UAE, especially when local credibility and fit matter as much as the deck itself.

Treat the data room as a speed tool

A clean data room shortens diligence. It also signals that the company is being run with discipline.

At minimum, prepare:

- Corporate documents such as incorporation records, cap table, and major approvals

- Commercial documents including customer contracts, pilot agreements, and partnership paperwork

- Financial files such as historical performance, assumptions, and forecast logic

- IP and compliance files that show ownership and reduce obvious diligence concerns

Google Drive is fine if the folder structure is clean. Notion works well as an index and context layer. DocSend is useful when you want controlled sharing for selected documents. The tool matters less than consistency.

Three habits make a visible difference:

- Keep file names clean and consistent.

- Remove stale versions before sharing.

- Make sure finance, legal, and product documents tell the same story.

That last point gets overlooked. In many UAE and wider MENA rounds, investor conviction is built meeting by meeting, then checked through references and diligence. If your deck says one thing, your model says another, and your contracts tell a third story, trust drops fast. A founder can recover from imperfect metrics. Recovering from avoidable inconsistency is much harder.

Targeting the Right Investors in the MENA Ecosystem

Founders waste a shocking amount of time pitching people who were never a fit.

The problem usually isn't effort. It's targeting. A key pitfall in the regional process is weak investor targeting, and guidance stresses focusing on investors with prior stage and sector fit because misaligned outreach wastes time and lowers conversion odds. It also highlights the value of warm introductions and evidence-backed metrics in practice, as explained in Carta's fundraising guidance for startups.

Build an investor list like you would build a sales pipeline

Don't start with the biggest names. Start with fit.

A useful investor screen includes:

- Stage fit. Do they invest where you are, not where you hope to be?

- Sector fit. Have they backed businesses with similar models or buyer types?

- Geography fit. Are they active in the UAE or wider MENA, or only vaguely interested?

- Behaviour fit. Do founders say they move clearly, add value, and communicate well?

Founder conversations matter. A fund's website tells you the story it wants to tell. Other founders tell you how it behaves when a process gets real.

What a good target list looks like

A weak list is long and flattering. A strong list is shorter and built around conversion.

Split targets into three groups:

| Group | What qualifies them |

|---|---|

| High priority | Strong stage, sector, and geography fit, plus realistic access path |

| Medium priority | Good fit on two dimensions, but less certainty on activity or timing |

| Low priority | Brand-name funds or angels with unclear relevance |

That structure stops you from spending prime weeks on low-probability conversations.

If you're researching who is active and what kind of investor may suit your company, this guide to finding the right investor in the UAE is a useful starting point.

Avoid reputation damage from spray-and-pray outreach

MENA is large, but the startup ecosystem is still connected. Broad, generic outreach travels fast. So does weak preparation.

A bad investor meeting doesn't just waste that meeting. It can close doors to the next introduction.

Good founders treat investor mapping like customer discovery. They build a view of the ideal investor profile, test assumptions, gather feedback from peers, and prioritise signal over volume.

That shift changes the whole startup fundraising process. It stops being a hunt for anyone with capital and becomes a search for the few people who can provide effective backing for this company at this stage.

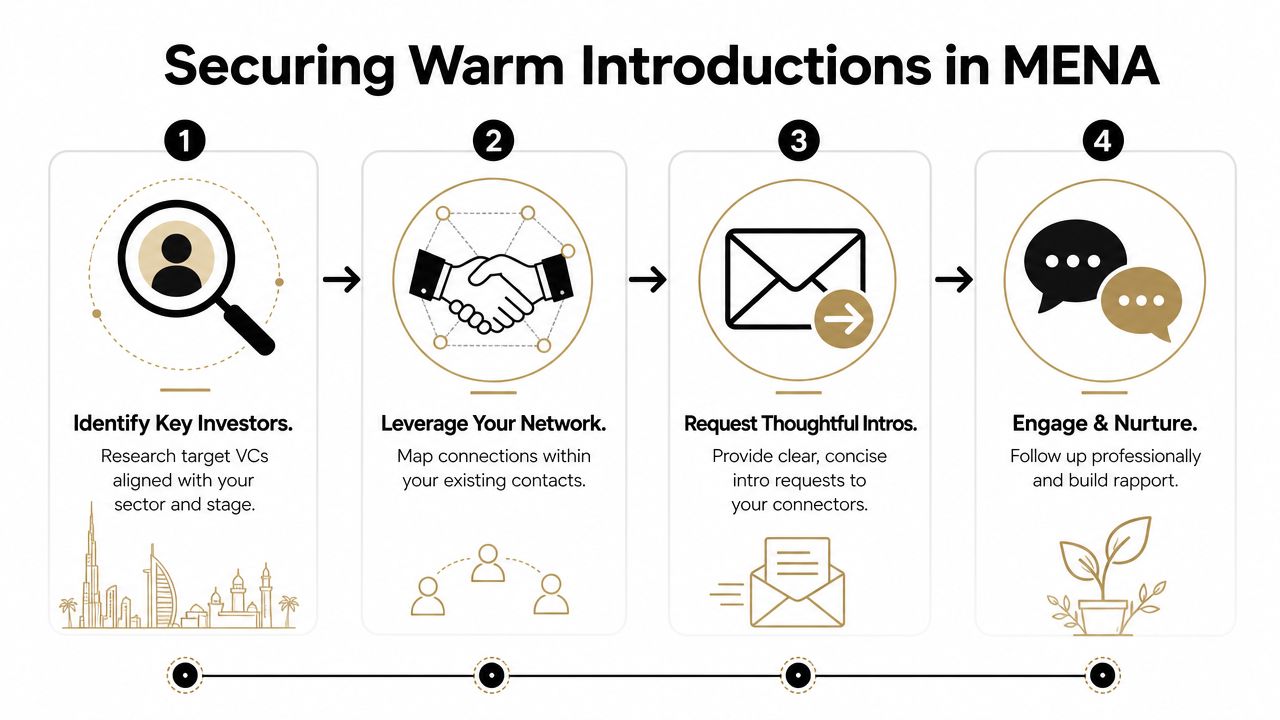

Executing Smart Outreach with Warm Connections

Outreach quality matters more than outreach volume. In the UAE, that's not a nice principle. It's how trust gets built.

Fundraising success in the UAE is less about pitching harder and more about building pre-raise trust, targeted investor alignment, and peer validation. In a market where investors are making fewer, higher-conviction bets, the quality of introductions and ecosystem trust matters more than broad outreach, as discussed in this fundraising perspective focused on investor alignment.

What weak outreach looks like

A first-time founder often writes something like this:

Hi, we're building an exciting startup in the region and would love to pitch. We're raising now and think you'd be a great fit. Are you free next week?

Nothing is technically wrong with that message. It just gives the investor no reason to care, no evidence of fit, and no trust transfer.

A better route is a double opt-in through someone the investor already respects. The connector sends a short note explaining why the match makes sense, and the founder follows up with a tight message that makes the next step easy.

Give your connector a forwardable note

When you ask for an introduction, do the work for the person helping you.

Send them:

- Who you want to meet and why that investor fits

- A two or three line company summary with stage and focus

- One sentence on traction or proof

- A clear ask such as an intro for a first conversation, not “please help me fundraise”

That's where a lot of founders fail. They ask for help in a way that creates work.

For a legal and practical view on approaching investors, Coto & Waddington's startup funding advice is worth reviewing alongside your outreach plan.

A useful lead-in before you start sending requests is this guide on breaking into top VCs with a warm introduction strategy for startups.

Run outreach like a managed process

Once intros start coming in, your job is to maintain momentum without looking frantic.

Use a simple operating rhythm:

- Track every conversation in one place. Airtable, Notion, or even a disciplined spreadsheet works.

- Send follow-ups quickly with the exact material requested.

- Share meaningful updates when something has changed, not every few days.

- Keep social proof tight. Mention relevant customers, angels, or founder references only when they strengthen credibility.

Here's a useful walkthrough before you draft your intro requests:

The real asset is borrowed trust

Warm intros work because they compress doubt. The investor still needs to believe the company, but they spend less time deciding whether to trust the conversation itself.

That's why founder communities, peer circles, and operator networks matter. One practical option in the UAE is Founder Connects, which organises founders into curated peer groups and facilitates relevant introductions. Used well, that kind of network can help founders pressure-test messaging, identify shared contacts, and avoid blind outreach.

The startup fundraising process gets easier when you stop trying to manufacture urgency and start building credibility through people who already know your work.

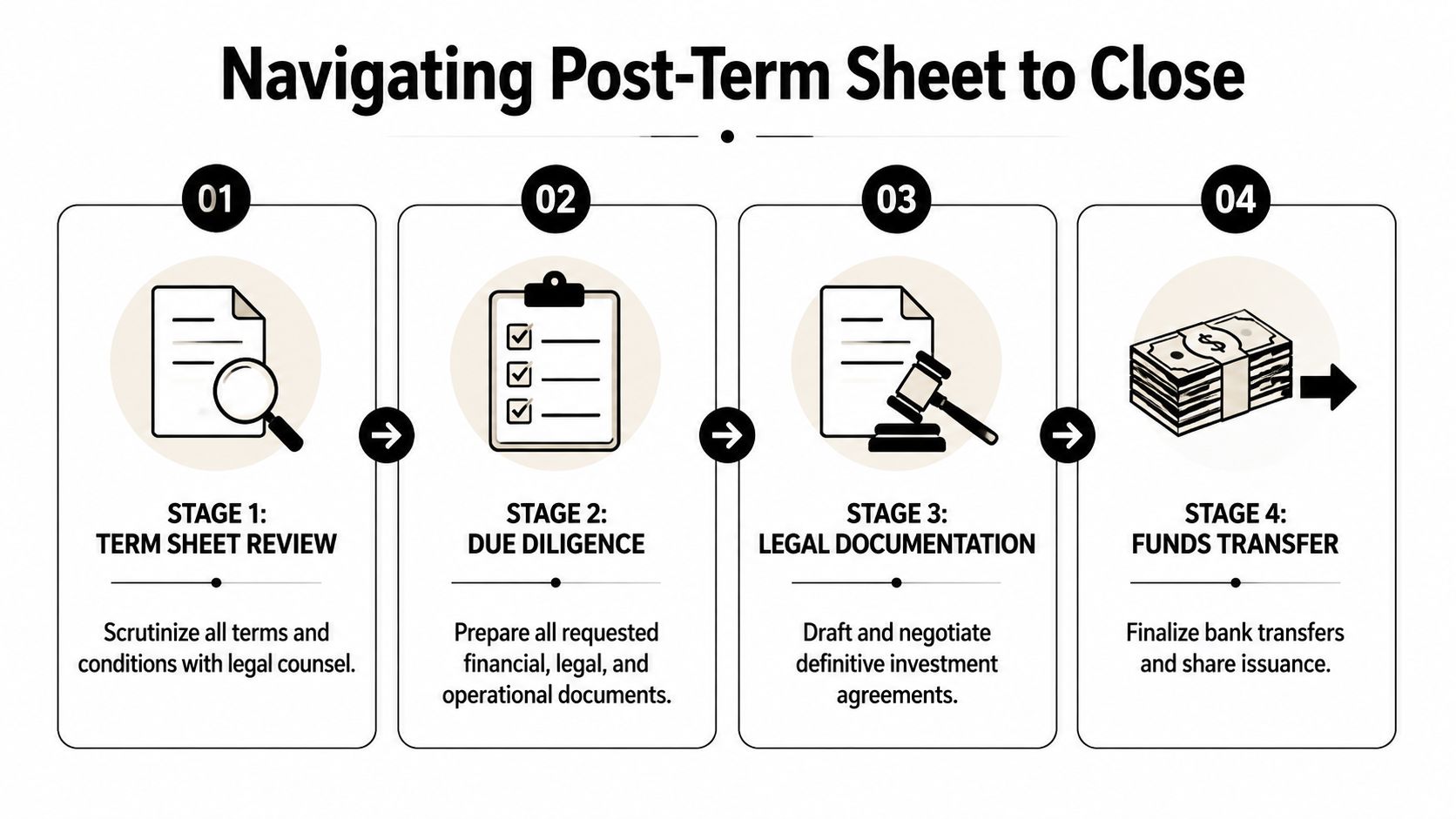

From Term Sheet to Closing Your Round

You finally get the call every founder wants. The investor says they are in, sends a term sheet, and asks legal to begin. In the UAE, that usually means the real scrutiny starts now.

A signed term sheet signals intent, not cash in the account. Closing can still slow down over diligence gaps, legal back-and-forth, or investor committee questions. In MENA, where conviction is often built through trusted relationships and peer validation, how you handle this phase affects more than the current round. People talk, and a messy close travels fast across the market.

Know what you are agreeing to

Seed founders often anchor on valuation and move too quickly through the rest. That is how expensive mistakes get signed.

Read the economic terms and the control terms with the same level of care. A strong headline valuation can still leave founders boxed in later if the preference stack is heavy, pro-rata rights are too broad, or consent rights make ordinary decisions harder than they should be.

Focus on the points that shape your next 18 to 24 months:

- Liquidation preference. This determines who gets paid first in an exit and how returns are split.

- Pro-rata rights. These affect who can maintain ownership in the next round and how much room remains for new investors.

- Control and governance terms. Board seats, founder vesting, reserved matters, and information rights all affect day-to-day operating freedom.

- Exclusivity and closing conditions. These define how long you are tied up and what still needs to happen before money moves.

Use counsel that can explain commercial impact in plain English. A practical question I always ask is: “What does this clause do to me in the next round if growth is slower than plan?” Good lawyers answer that directly.

Diligence exposes operating discipline

Once a lead investor commits, they start checking whether the company underneath the story is investable.

That review usually covers corporate records, cap table accuracy, financial controls, customer contracts, employment documents, regulatory exposure, and IP ownership. If one founder wrote early code through a side entity, if contractor IP was never assigned properly, or if SAFEs and side letters do not match the cap table model, expect delay.

I have seen founders lose weeks on issues that were fixable in a day if handled earlier.

A clean data room improves confidence because it shows the company is run with care. Orrick's overview of startup fundraising documents is a useful reference for the legal paperwork founders are commonly expected to organise during financing and closing: Orrick guide to startup financing documents.

| Diligence area | What founders should have ready |

|---|---|

| Corporate | Incorporation records, shareholder approvals, cap table, prior financing documents |

| Commercial | Signed customer contracts, partner agreements, revenue concentration notes |

| Financial | Historical financials, bank records, forecast assumptions, burn logic |

| Legal and IP | IP assignments, trademark filings, software licences, key obligations |

| Team | Employment agreements, contractor documentation, ESOP records |

Keep the process tight until funds land

Closing risk stays alive until documents are signed and the wire hits.

Founders should run this phase with discipline:

- Answer diligence requests fast, but only after checking accuracy

- Keep the round architecture clear so all parties understand who is leading, who is following, and what is still open

- Maintain contact with other interested investors until closing is complete

- Disclose known issues early with context and a fix, rather than letting counsel discover them late

- Stay close to local legal mechanics if the structure spans UAE mainland, ADGM, DIFC, or an offshore parent entity

That last point matters more in MENA than generic fundraising guides admit. Cross-border structures, nominee arrangements, and entity setup choices can create friction if no one has mapped them properly before documents start circulating.

Investors notice the quality of the close. A founder who handles pressure well, keeps documents clean, and resolves issues without drama gives the market a reason to trust the next milestone too.

Life After the Wire Transfer Your Post-Funding Plan

The wire transfer changes your bank balance. It doesn't solve execution.

After the round closes, the best founders switch quickly from fundraising mode to operating mode. They don't disappear for months. They turn investor promises into a working cadence.

Onboard investors properly

A new investor who only hears from you during emergencies won't be very useful.

Set expectations early:

- Send a regular update with progress, challenges, key asks, and major decisions

- Create a clean reporting rhythm so investors know when they'll hear from you

- Use specific requests when you want help with hiring, partnerships, customer intros, or follow-on strategy

Relationship depth starts paying back at this point. Investors can be helpful when founders give them enough context to act.

Turn use of funds into an operating plan

A lot of teams raise against a milestone, then drift into opportunistic spending.

Don't do that. Translate your use-of-funds slide into a clear internal plan with owners, hiring decisions, product priorities, and review dates. If the round was meant to get the company to the next meaningful proof point, every major spend should connect back to that.

A practical way to run this is to keep one internal document that tracks:

- the milestone the round was raised for

- the assumptions behind hiring and burn

- the risks that could push the company off plan

- the evidence you'll need for the next round

Start preparing for the next raise early

The next round starts much earlier than most first-time founders expect.

Not with a deck. With behaviour.

Investors in later rounds want to see consistency. They want clean reporting, credible decision-making, and signs that this team can absorb capital without losing focus. That means your board and investor updates aren't admin. They are part of future fundraising readiness.

Good post-funding discipline creates the story of the next round before you ever reopen the deck.

This is also where founder isolation becomes expensive. Post-round, many teams get consumed by hiring, product, and firefighting. They lose the outside perspective that helped them make clear decisions during the raise. Staying close to founder peers helps keep perspective when plans slip, hires miss, or investor pressure starts creeping in.

The startup fundraising process is easiest to understand backwards. The best raise is the one that leaves the company sharper after the money arrives, not just relieved on closing day.

If you want a more structured way to prepare for a raise, pressure-test your story, and get closer to the right founders and ecosystem relationships, Founder Connects offers a UAE-based community built around curated peer groups, practical support, and relevant introductions.

Building in MENA? You don't have to do it alone.

Join 300+ founders in the Founder Connects Residency. Monthly squad calls, warm intros, $3M+ in perks, and much more. All for less than your monthly coffee budget.

Popular posts

The premier community for tech founders, investors, and builders. Connect, collaborate, and grow together.