UAE Corporate Tax for Startups Explained: 2026 Guide

Building in MENA? You don't have to do it alone.

Join 300+ founders in the Founder Connects Residency. Monthly squad calls, warm intros, $3M+ in perks, and much more. All for less than your monthly coffee budget.

You've probably had some version of this conversation already.

A founder asks, “We're still tiny. Do we owe tax now?” Someone else says, “Free zone means zero anyway.” Their accountant sends a long note full of defined terms, elections, qualifying income, de-minimis tests, and filing dates. Everyone nods. Almost nobody feels clearer.

That's why most explainers on UAE corporate tax miss the point. Founders don't need more jargon. They need the plain-English version of UAE corporate tax for startups explained by someone who cares about what breaks in real life: cash flow, messy books, wrong assumptions, missed filings, and free zone setups that aren't as simple as the brochure made them sound.

When corporate tax hit, the biggest lesson was this: the UAE didn't stop being founder-friendly. But the margin for sloppy admin got smaller. If you understand the rules early, you can stay efficient. If you wing it, tax becomes one more preventable distraction.

Is the Party Over for UAE Startups

A founder closes a seed round, signs a free zone package, and assumes tax can wait until the business is bigger. A few months later, the finance cleanup starts. Invoices are inconsistent, expenses are sitting in the wrong buckets, and nobody is fully sure whether the company needed to register earlier. That is a significant shift.

The UAE still gives startups a strong base to build from. What changed is the old habit of treating tax as background noise. The federal corporate tax regime took effect for financial years starting on or after 1 June 2023, as set out by the UAE Ministry of Finance corporate tax overview. For many early-stage companies, the headline rate is not the immediate problem. The operational discipline is.

That is the part accountants often underplay. Founders usually do not get hurt first by a large tax payment. They get hurt by messy books, wrong assumptions about free zone status, missed registrations, and finding out too late that a simple setup choice created extra admin.

What changed for founders

Three practical shifts matter:

- Corporate tax is now part of company setup, not a later-stage problem. You need a tax position from the start, even if your payable tax is low or nil.

- A low tax bill can still come with real compliance work. Registration, records, and filing deadlines do not disappear because the business is small.

- Free zone marketing is not the same as free zone tax treatment. The brochure says one thing. Your actual customers, income type, and structure decide the outcome.

I have seen founders focus on the 9 percent headline and miss the bigger risk. The expensive mistakes usually happen before the first payment is due.

The useful founder view

Treat corporate tax the same way you treat payroll, VAT, or basic finance controls. It is now part of running a proper UAE company. The good news is that this is manageable if you get ahead of it. The bad news is that it becomes annoying and costly when you leave it until your first filing reminder.

Start with four questions:

- Are we looking at taxable profit, or are we casually reacting to revenue numbers without understanding the difference?

- Does our free zone or mainland setup still fit the way we earn money today?

- Are our books clean enough that a return can be prepared without a last-minute reconstruction exercise?

- Are we assuming a tax benefit that depends on conditions we have not checked properly?

That is the founder lens that matters. The UAE advantage is still there. The era of casual assumptions is not.

The Core Rule The 9 Percent Threshold

A lot of founders hear “9% corporate tax” and assume the business becomes taxable the moment money starts coming in. That is the wrong starting point.

The UAE corporate tax regime taxes taxable profit, not revenue. For most businesses under the standard regime, the rate is 0% on taxable profit up to AED 375,000 and 9% on taxable profit above AED 375,000, as set out by the Federal Tax Authority's corporate tax guidance.

What matters in practice is simple. A startup can post healthy sales and still owe little or no corporate tax if margins are thin, hiring is heavy, or product costs are high. Another startup can have modest revenue and still hit taxable profit faster than expected because software margins are strong.

That is why founders get into trouble when they track tax risk from Stripe screenshots, bank balances, or invoice totals. The number that matters is profit after allowable business costs, adjusted properly for tax.

The threshold is tiered, not a cliff

Crossing AED 375,000 does not mean all your profit gets taxed at 9%.

Only the portion above that threshold falls into the 9% band. If your taxable profit is AED 500,000, the first AED 375,000 stays at 0% and only the remaining AED 125,000 is taxed at 9%. The Ministry of Finance corporate tax overview makes that structure clear, but many startup teams still budget for it incorrectly.

I have seen founders delay hiring because they thought one profitable quarter would suddenly make the whole year “fully taxable.” That is not how the rule works. The better question is whether your bookkeeping is clean enough to calculate taxable profit accurately before you start making decisions off a rough estimate.

Small Business Relief matters more than many early-stage founders realise

For a lot of startups, the more useful rule is Small Business Relief, not the headline tax band.

The relief is available to eligible resident taxable persons with revenue of AED 3 million or below for the relevant tax periods, subject to conditions and the current availability window, under Cabinet Decision No. 73 of 2023 on Small Business Relief. If you qualify and elect to use it, you are treated as having no taxable income for that period.

That sounds generous, and for many bootstrapped or early revenue startups it is. But founders should not treat it as automatic. Reliefs usually work well only when someone has checked the conditions, documented the position, and reflected it properly in the filing.

The Federal Tax Authority also spells out the Small Business Relief conditions and election mechanics. Read that before you assume your accountant will “handle it.”

The practical founder version

Three mistakes come up all the time:

- treating revenue as if it were taxable profit

- assuming the 9% rate applies to the full profit once the threshold is crossed

- assuming Small Business Relief applies by default without confirming eligibility and making the right election

A simple internal tax note fixes most of this. Ask for one page showing current revenue, estimated taxable profit, whether Small Business Relief is available, and what has to be elected or disclosed. If your company is still deciding between mainland and free zone for a tech business, this comparison of UAE free zones for tech startups is worth reviewing alongside the tax position, because structure and tax treatment usually drift together as the business changes.

The founders who stay out of trouble are rarely the ones with the smartest tax theory. They are the ones who get the numbers clean early and stop guessing.

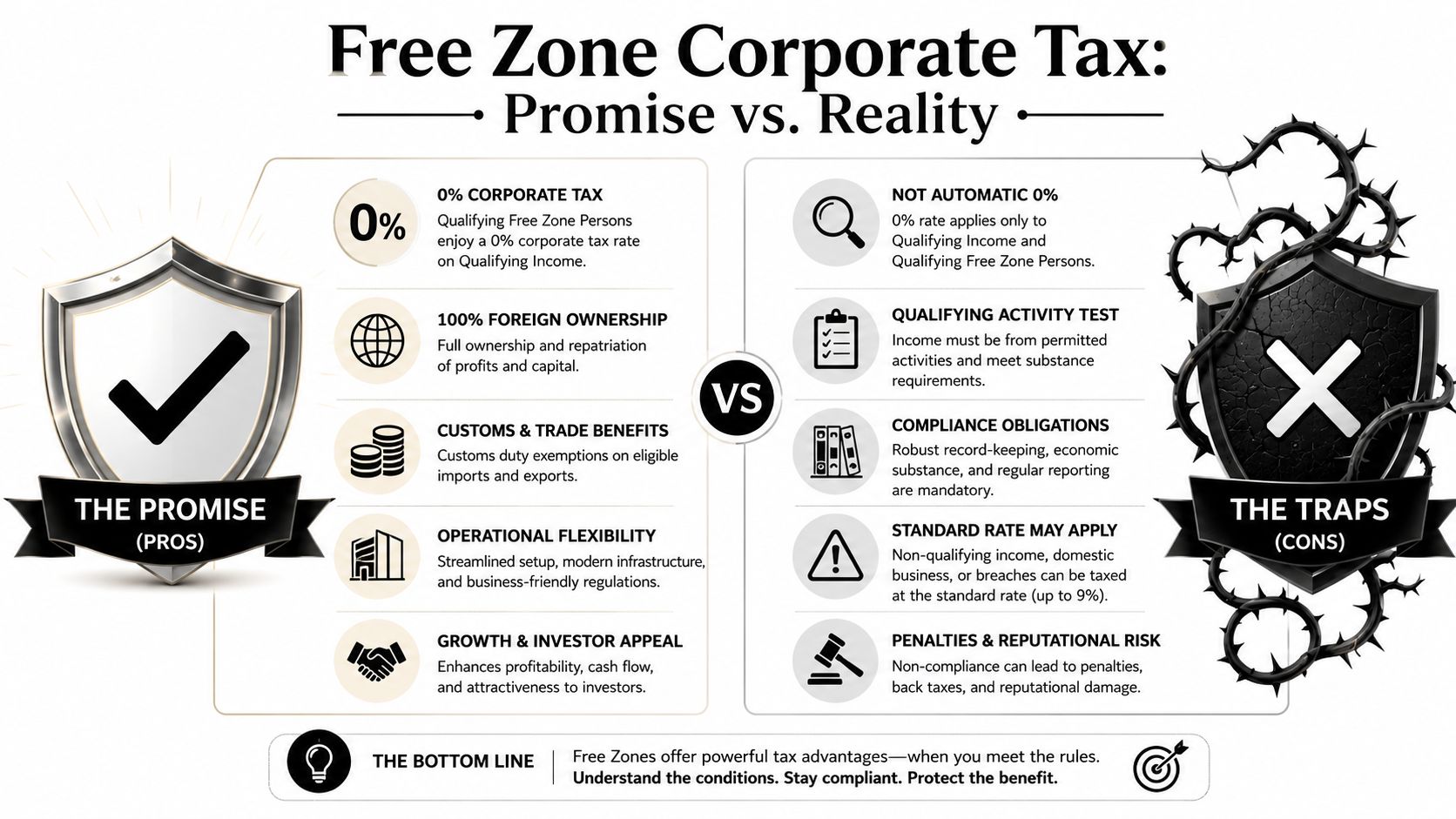

Free Zone Tax The 0 Percent Promise and Its Hidden Traps

A lot of founders learn this one late. They picked a free zone, heard “0% tax,” and assumed the hard part was over. Then the business starts selling in ways the original setup never really considered.

A UAE free zone company can still access a 0% corporate tax rate on qualifying income, but only if it meets the conditions to be a Qualifying Free Zone Person. That includes substance, compliance with transfer pricing rules where relevant, proper income classification, and staying within the permitted limits for non-qualifying income, as set out in the PwC summary of the UAE Free Zone corporate tax rules.

The phrase that matters is qualifying income. Founders get into trouble when they treat the free zone licence itself as the tax benefit.

The trap accountants sometimes mention too late

The de minimis rule is where a lot of startup tax plans break.

If your non-qualifying revenue goes over the allowed limit, you can lose Qualifying Free Zone Person status. In plain English, one messy revenue stream can do more damage than founders expect. The FTA's corporate tax materials and the Cabinet framework make this a technical test, but the startup version is simple. If you are mixing revenue types without tracking them properly, you are taking a real risk.

I have seen this happen with software startups that begin with clean cross-border SaaS revenue, then add side services for mainland customers because the sales cycle is faster and the cash helps. Commercially, that can be a smart move. Tax-wise, it can be an expensive one if nobody has mapped what that new income does to your free zone position.

A practical example

Say your company is in a free zone and sells software subscriptions to overseas clients. Fine.

A few months later, the team adds implementation work, local consulting, or direct mainland projects. Those deals may look small against total revenue, but they can change the classification of income and push you into a position you did not intend. The painful part is that founders usually notice this after contracts are signed and invoices are issued, not before.

That is why free zone tax planning is really revenue design, not office-location trivia.

| Scenario | Startup A (Disciplined) | Startup B (Exposed) |

|---|---|---|

| Revenue model | Defined upfront by income type | Expanded informally as sales opportunities appeared |

| Mainland business | Reviewed before contracts are signed | Accepted case by case without tax review |

| Bookkeeping | Income tagged clearly by stream and customer type | Revenue grouped too broadly to test exposure |

| Tax position | Better chance of keeping 0% on qualifying income | Higher risk of losing free zone treatment |

What to check before you call yourself “0% tax”

Founders should review four things, and review them early:

- Who the customer is: foreign, free zone, mainland, related party

- What you are selling: product revenue, service revenue, licensing, consulting, support

- Whether your operations support the tax position: people, costs, decision-making, and actual activity in the UAE

- Whether finance can track income properly: monthly, by line of business, not once a year in a panic

This is also where a decent advisor earns their fee. Good accountants do more than produce filings. They help set up controls, challenge bad assumptions, and flag risks before they become expensive. This short piece on how accountants help small businesses is UK-focused, but the point carries over. Founders need an accountant who asks how the business makes money, not just one who posts entries.

If you are still deciding where to set up, or whether your current structure matches how your startup sells, this comparison of UAE free zones for tech startups is useful. The cheapest free zone is not always the safest choice once your revenue model gets more complicated.

The free zone advantage is still real. The catch is that it rewards startups with clear revenue boundaries and decent financial discipline. If your company is still experimenting heavily with offers, customer segments, and mainland sales, treat the 0% promise as conditional from day one.

From Theory to To-Do List Audits Deadlines and Registration

A lot of founders hit the same point. They understand the headline rule, then realise the primary risk is not the tax rate. It is missing a registration, filing late, or discovering their books cannot support the position they planned to take.

That is the part accountants sometimes underplay. Corporate tax in the UAE is manageable for startups, but only if someone owns the admin properly from the start.

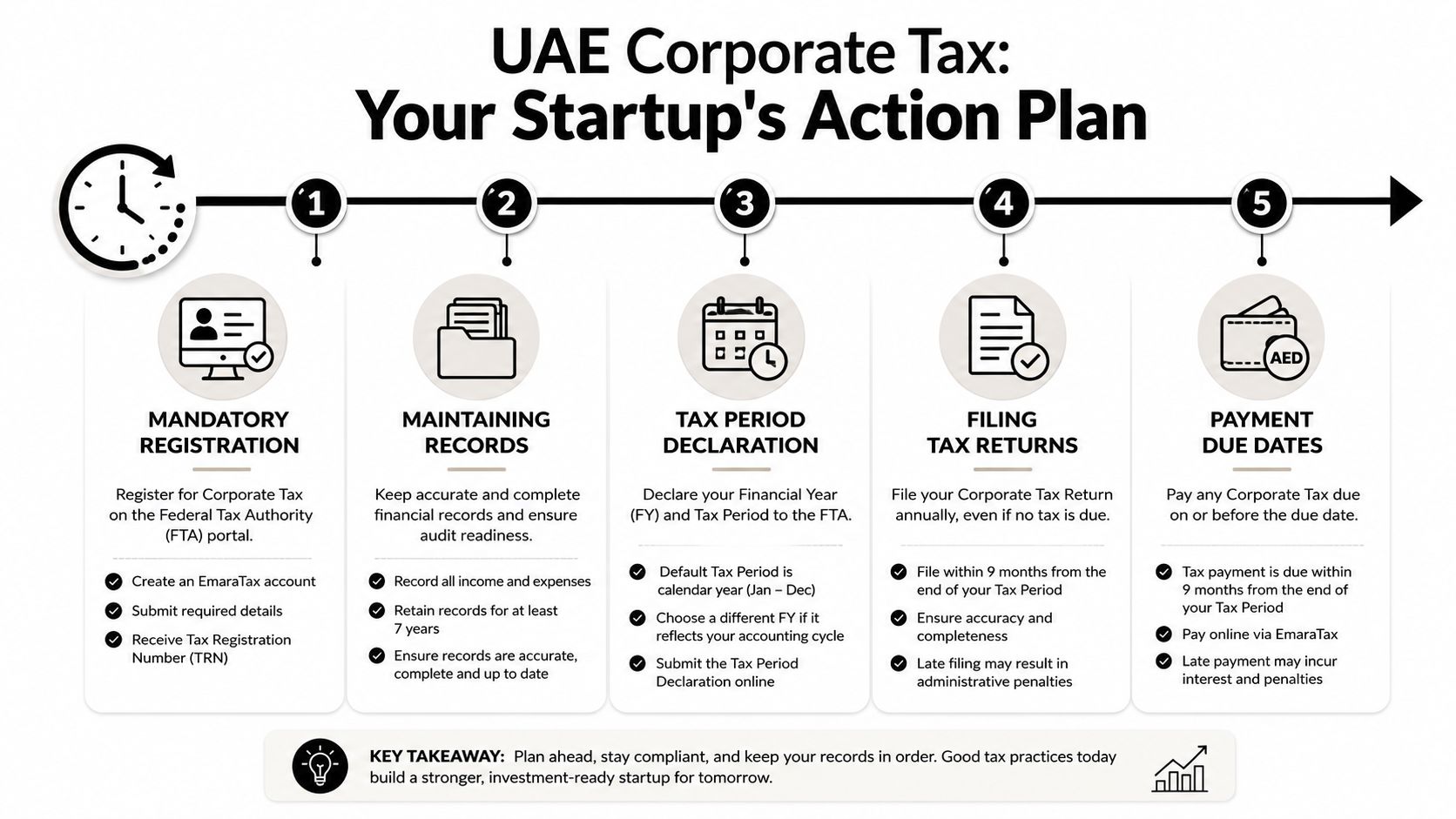

The baseline obligations are straightforward. Register through EmaraTax, keep proper accounting records, file an annual corporate tax return, and track your deadline based on your financial year-end. The Federal Tax Authority sets the filing deadline by reference to the end of the relevant tax period, so founders should confirm their exact dates directly on the FTA's corporate tax page rather than relying on memory or WhatsApp advice.

The founder checklist

Handle these in order:

Register early

Do not wait for profitability. Tax registration and tax liability are related, but they are not the same operational question.Close your books every month

If revenue, costs, and founder reimbursements are only sorted once a year, filing becomes slow, expensive, and far more error-prone.Confirm your tax period

Your filing deadline follows your financial year-end. Put the date in the calendar now, with reminders well before it becomes urgent.Keep support for judgment calls

If you are relying on a free zone position, small business relief, or a specific treatment for intercompany charges, keep the contracts, workings, and internal approvals together.

What an audit usually looks like

For an early-stage startup, an FTA review is usually a records exercise.

The practical question is simple. Can you show how the numbers in your return tie back to financial statements, invoices, contracts, bank movements, and the tax treatment you chose? If yes, the process is usually manageable. If no, even a simple startup can start to look careless.

I have seen founders spend weeks fixing problems that were avoidable with one monthly finance review and a clean document trail.

The setup that saves time later

A workable setup is not complicated, but it does need discipline:

- Cloud bookkeeping software so records are not split across spreadsheets, inboxes, and personal chats

- A document folder by tax year for contracts, invoices, board approvals, and FTA correspondence

- A short monthly finance review between the founder and accountant to catch issues while they are still small

- A written note for unusual items such as related-party charges, shareholder expenses, or revenue that may affect tax treatment

Good accountants matter here because they build process, not just filings. This article on how accountants help small businesses is not UAE-specific, but the point is right. A useful accountant does more than submit returns. They help founders keep records in a shape the tax position can survive.

If finance still sits half in Xero and half in someone's inbox, this guide to startup accounting in the UAE is a practical place to tighten the basics.

One habit that prevents panic

Put your tax filing date, monthly close date, and internal tax review date into the same founder ops calendar as payroll, VAT, and licence renewals.

That one habit catches more mistakes than founders expect.

Common Mistakes That Will Cost You Money

The expensive mistakes are usually operational, not technical.

A founder hears "0% tax" from a setup agent, stays heads-down on product and sales, and only looks at the tax position when a bank, investor, or auditor asks for clean numbers. By then, the fix is slower, more expensive, and usually more awkward than it needed to be.

Mistake one believing the licence decides everything

Founders often treat the licence as the tax answer. It is not.

What matters is what the company does, who it sells to, and whether that activity still fits the conditions behind any preferential treatment. I have seen startups assume their Free Zone status protects everything, then discover too late that mainland revenue, non-qualifying income, or a bad understanding of the De Minimis rule changed the outcome. The licence got them set up. It did not keep them compliant.

Mistake two skipping registration because profit is low

Early-stage founders make this mistake for a simple reason. They confuse tax payable with tax obligations.

A startup can be loss-making and still need to register, keep proper records, and file on time. Waiting until the business is "big enough" usually creates a backlog, and backlog is where penalties and rushed accounting fees start to appear.

Mistake three books that are too messy to defend

This shows up everywhere. Revenue timing is unclear, expense support is missing, founder loans are not documented properly, and reimbursements sit in WhatsApp instead of the accounting file.

Poor books do more than make filing unpleasant. They weaken your position if the FTA asks questions, they slow diligence, and they make it harder to use reliefs cleanly. If your startup is investing in product or technical work, keep records that also support claims tied to UAE startup R&D incentives and government tax credits. Good documentation gives you options. Weak documentation removes them.

Weak books do not stay a finance problem. They become a fundraising problem, a diligence problem, and eventually a founder-trust problem.

Mistake four mixing personal and company spending

This starts as convenience. It ends as reconstruction.

A founder pays a supplier personally, the company covers a personal bill "just this once", and nobody records the entries properly. Later, those transactions have to be explained, classified, and supported. Some will be legitimate. Some will not survive scrutiny. Clean separation from month one is cheaper than sorting out twelve months of blurred spending under deadline pressure.

Mistake five forgetting to elect for Small Business Relief

Small Business Relief does not apply by magic. If you qualify, you need to make the election properly.

That point gets missed more often than it should, especially by founders who assume a low-revenue company will be treated automatically as outside the practical burden of corporate tax. The Federal Tax Authority's guidance on Small Business Relief is the place to confirm the conditions and mechanics. The trade-off is straightforward. The relief can reduce immediate tax friction, but founders still need books, deadlines, and eligibility checks handled properly.

A short review that catches most of this

Use these questions before each year-end and again before filing:

- Have we registered, and do we know the actual filing deadline?

- Has any revenue mix changed, especially mainland sales or income streams that may affect Free Zone treatment?

- Are founder expenses, reimbursements, and loans recorded clearly and supported?

- If we qualify for Small Business Relief, has the election been confirmed properly rather than assumed?

- Are we using outsourced employment or operating structures that shift tax exposure in ways the team has not examined?

That last point matters more than founders think. If your team uses outsourced staffing or cross-border employer structures, read up on the legal risks of PEO tax liability. Many startup tax issues begin with a shortcut that felt operationally convenient and turned out to carry legal and tax consequences nobody had priced in.

The Honest Take Does This Kill the UAE Advantage

A founder closes a seed round, hires fast, and assumes the UAE tax story is still simple. Then the first proper year-end arrives. The surprise is usually not the rate. It is the admin, the record-keeping, and the number of decisions that were left on autopilot.

My view is straightforward. The UAE still works well for startups. It just no longer rewards casual finance habits.

Why the advantage still holds

The old pitch was easy to sell because founders could focus on setup speed, low direct tax pressure, and regional access. That part has not disappeared. What changed is that corporate tax now forces earlier discipline, especially once a company starts generating real revenue, operating across mainland and Free Zone structures, or preparing for investor diligence.

That is a healthy change for some startups and an annoying one for others.

If your company is small, pre-profit, or still testing distribution, the tax cost itself may remain limited because of the reliefs discussed earlier. The main trade-off is operational. You need cleaner books, clearer expense policies, and someone in the business who understands how your structure affects tax treatment. Founders who treat this as a minor back-office issue usually end up paying more in accounting fixes, missed planning options, or restructuring later.

Where founders get the UAE advantage wrong

The mistake is not believing tax exists. The mistake is assuming the headline promise tells the whole story.

A Free Zone startup can still be in a very good position, but only if it protects that position carefully. The law now rewards founders who know exactly where revenue comes from, which entity signs contracts, and whether a side activity could taint the wider tax treatment. The PwC UAE corporate tax overview is useful on that point because it explains how exemptions and qualifying treatment sit on top of compliance requirements rather than replacing them.

That layered setup is the main point. The UAE did not lose its edge. The edge shifted from "low-tax by default" to "low-tax if you set it up properly and keep it clean."

What still makes the UAE attractive

Corporate tax is only one line in the decision.

Founders still choose the UAE because it is a practical base for selling across MENA, meeting investors, hiring internationally, and building with decent infrastructure around banking, logistics, and professional services. Investors also tend to prefer companies that operate inside a credible tax system with records they can review, rather than a business that says, "we thought none of this applied to us."

That matters more as you grow. A messy tax position rarely kills an early startup, but it does slow down diligence, increase legal costs, and create awkward conversations during funding or acquisition talks.

My honest founder view

The UAE is no longer a place where you can ignore corporate tax without consequences. For serious founders, that is manageable.

A 9 percent rate above the relevant threshold is still reasonable by international standards. The bigger risk is not the tax bill. It is losing a relief, misreading Free Zone conditions, or discovering too late that your operations outgrew the structure you started with. Founders should also keep an eye on related planning areas, such as research and development incentives for UAE startups, because tax efficiency now comes more from good structuring than from broad assumptions.

My bottom line is simple. The UAE remains a strong place to build, especially for startups with regional ambition. The founders who benefit most now are the organised ones.

If you want founder-level help making sense of operational decisions like tax setup, accounting processes, and growth trade-offs, Founder Connects is a practical place to meet other UAE and MENA founders working through the same questions in a more honest, execution-focused way.

Building in MENA? You don't have to do it alone.

Join 300+ founders in the Founder Connects Residency. Monthly squad calls, warm intros, $3M+ in perks, and much more. All for less than your monthly coffee budget.

Popular posts

The premier community for tech founders, investors, and builders. Connect, collaborate, and grow together.